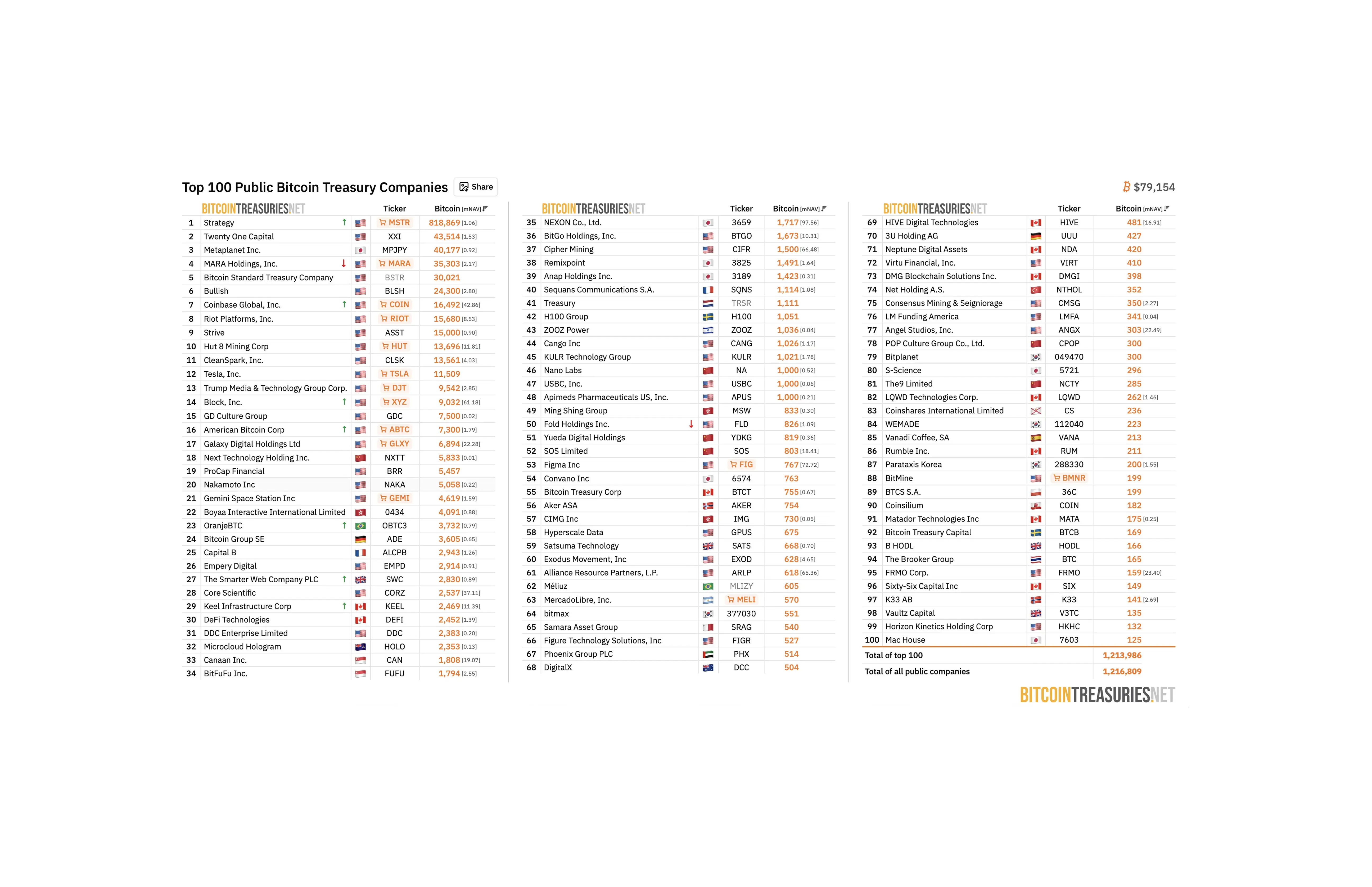

Quick summary

Four parallel systems emerge in 2026: TradFi, CeFi, DeFi, and Bitcoin, each distinct

TradFi, CeFi, and DeFi coordinate financial activity, while Bitcoin focuses on monetary settlement

TradFi, CeFi, and DeFi increasingly converge via blockchain, compliance, and real-world asset tokenization

Bitcoin remains structurally separate as fixed-supply, self-custodied, censorship-resistant monetary infrastructure the layer institutions are building around

Modern finance increasingly runs across several parallel financial rails.

In 2026, capital moved across four separate systems: Traditional Finance (TradFi), Centralized Finance (CeFi), Decentralized Finance (DeFi), and Bitcoin. Each approach settlement, custody, and trust through different infrastructure models. TradFi built institutional coordination through banks, regulators, and legal systems. CeFi simplified access to digital assets through centralized platforms. DeFi moved financial activity onto programmable blockchain rails. Bitcoin introduced decentralized monetary settlement independent from institutional liability structures, where assets remain outside centralized freeze controls.

This article explains how the four systems differ, where they increasingly overlap, and why Bitcoin continues operating differently from the rest of the financial stack.

How Modern Finance Split Into TradFi, CeFi, DeFi, and Bitcoin

Three systems compete around financial coordination. Bitcoin competes around money itself.

TradFi: Institutional finance coordinated through banks, brokers, regulators, and payment networks

CeFi: Centralized crypto platforms simplifying digital asset access and liquidity

DeFi: Smart contract protocols executing financial logic directly on blockchain infrastructure

Bitcoin: A decentralized monetary network optimized for scarcity, settlement, and self-custody

TradFi: Institutional Capital and Regulatory Coordination

Traditional Finance remains the largest financial system by assets under management because institutions require legal enforceability, predictable settlement, and deep liquidity pools. Governments, pension funds, sovereign wealth funds, insurers, and corporations still operate primarily through TradFi rails.

The system traces back to 14th-century Florence, where the Medici Bank formalized double-entry bookkeeping, branch networks, and bills of exchange. The operational templates that still underpin modern banking. Every major financial innovation since, from central banking to clearinghouses to electronic settlement, has been built on that foundation rather than replacing it.

That 600-year institutional continuity is the source of TradFi's strength and its constraint. The infrastructure is deeply trusted but structurally slow to integrate with anything built outside it.

TradFi Strengths:

Regulatory coordination: Institutions operate inside established legal and accounting frameworks

Deep liquidity: Traditional markets control the largest pools of global capital

Consumer protection: Fraud systems, dispute resolution, and insured deposits reduce operational uncertainty

Institutional credibility: Banks and regulated custodians remain integrated into corporate and sovereign finance

The practical benefit is predictability. Large institutions managing billions prioritize operational stability over censorship resistance or decentralization.

TradFi Risks:

Slower settlement infrastructure: International transfers and institutional reconciliation still involve delays and intermediaries

Restricted global access: Large portions of the world remain excluded from banking infrastructure

Monetary expansion: Fiat currency supply remains tied to central bank policy

Legacy system friction: Older infrastructure struggles integrating with blockchain-native settlement systems

This explains accelerating institutional interest in stablecoins, tokenized treasuries, blockchain settlement rails, and programmable asset infrastructure.

TradFi Main Players

Traditional Finance increasingly adopts blockchain settlement infrastructure while maintaining centralized coordination. Some examples include:

BlackRock: BlackRock launched BUIDL, a tokenized treasury fund originating on Ethereum, and became the largest Bitcoin ETF issuer through its iShares product

JPMorgan: Operates Kinexys, a blockchain settlement network processing institutional dollar transfers, and recently tokenized its first private equity fund on-chain

Goldman Sachs: Operates GS DAP (Goldman Sachs Digital Asset Platform), a proprietary blockchain infrastructure used to tokenize money market funds in a joint launch with BNY in July 2025.

Fidelity: Launched three live blockchain products FDIT (Fidelity Digital Interest Tokenized Treasury Bills), a tokenized US Treasury fund on Ethereum; FIDD (Fidelity Digital Dollar), a GENIUS Act-compliant stablecoin issued by Fidelity Digital Assets NA, a federally chartered national trust bank, targeting 24/7 institutional settlement and on-chain retail payments. As well as the FYOXX (Fidelity Treasury Digital Fund), a tokenized money market fund backed entirely by US Treasury securities and cash.

CeFi: The Bridge Between Banking and Crypto

Centralized Finance became the operational gateway connecting traditional capital with digital asset markets. Coinbase was founded in 2012 by Brian Armstrong and Fred Ehrsam, Kraken launched its exchange in 2013 after being founded in 2011, and Binance was founded in 2017 by Changpeng Zhao, growing from a startup into the world's largest exchange by volume in under a year.

Three platforms that simplified crypto onboarding by abstracting away blockchain complexity and building the fiat on-ramps that brought the first wave of retail and institutional capital into digital assets.

CeFi Advantages:

Simplified user experience: Digital asset access became easier for retail and institutional participants

Fiat connectivity: Users move capital directly between banking systems and crypto markets

Liquidity aggregation: Centralized exchanges concentrate global trading activity into deep order books

Institutional access: Funds and corporations enter digital asset markets through regulated custodians and compliance structures

Most capital entering crypto still flows through CeFi infrastructure first before interacting with decentralized systems.

CeFi Risks:

Counterparty exposure: Users depend on platform solvency and operational integrity

Custodial vulnerability: Centralized wallets create concentrated attack surfaces

Regulatory dependence: Exchanges remain exposed to jurisdictional restrictions and licensing pressure

Liquidity contagion: Failures inside large firms spread rapidly across interconnected markets

The collapses of FTX, Celsius, BlockFi, and Genesis demonstrated how centralized leverage and opaque liabilities destabilize broader market liquidity conditions. The sector has shifted toward proof-of-reserves, compliance integration, segregated custody structures, and institutional-grade reporting, accelerated by the 2022 exchange collapses and the subsequent passage of MiCA in the EU and the GENIUS Act in the US.

DeFi: Programmable Financial Infrastructure

DeFi transformed blockchains from payment systems into financial operating systems. Instead of banks coordinating lending, trading, and collateral management, smart contracts execute financial logic directly on-chain. Protocols such as Aave, Uniswap, and Pendle function as modular financial infrastructure layers rather than isolated applications.

DeFi Advantages:

Permissionless access: Wallet holders globally interact with protocols directly

Transparent infrastructure: Reserves, collateral, and transaction flows remain publicly auditable

Programmable yield markets: Financial products structured directly through smart contracts

Composable capital systems: Lending, trading, derivatives, and collateral layers integrate together

The Pendle ecosystem reflects this transition precisely. Pendle splits yield-bearing assets into principal tokens and yield tokens, enabling fixed and variable yield trading on a single AMM. In May 2026, Pendle pools wrapping yield from Strategy's STRC preferred stock — via Saturn's sUSDat and Apyx's apyUSD — were paying 16–18% annualized yield while standard stablecoin pools sat near 5%. Michael Saylor referenced the ecosystem directly at Consensus 2026.

Yield has begun trading as a standalone financial instrument, mirroring stripped fixed-income structures in traditional markets.

That composability is also where fragility concentrates.

DeFi Risks:

Smart contract vulnerabilities: Exploits can impact billions in collateral with no recourse mechanism

Governance coordination: Emergency responses depend on protocol treasury depth, voting structure, and response speed, as demonstrated by Aave's governance reaction to the Kelp DAO and LayerZero exploit, where interconnected restaking collateral created rapid stress across lending markets

Bridge dependencies: Cross-chain infrastructure increases operational complexity and attack surfaces

Liquidity fragility: Collateral stress transmits rapidly across composable protocol layers

Audit gaps: BlackRock's BUIDL held $2.5 billion across eight blockchains as of April 2026, with only 0.75% actively deployed in DeFi protocols across two chains, Ethereum ($15.6M) and Polygon ($3.2M), with the remaining six chains sitting at zero deployment, reflecting institutional caution toward smart contract risk

The industry has shifted toward infrastructure auditing frameworks that test real usage, protocol revenue margins, crisis performance, and whether liquidity is earned or incentive-rented.

Bitcoin: Decentralized Monetary Infrastructure

Bitcoin occupies a different category from the rest of the financial stack.

TradFi, CeFi, and DeFi coordinate financial activity. Bitcoin coordinates monetary settlement. That distinction is sharpening. Engineered with a fixed supply of 21 million coin, Bitcoin functions as a long-term savings instrument designed to preserve purchasing power against the structural debasement of fiat currencies, a property no other layer in the financial stack was built to provide.

Bitcoin Advantages:

Fixed supply: Monetary issuance capped at 21 million coins

Decentralized settlement: Transactions settle through a globally distributed network without institutional intermediaries

Self-custody: Holders maintain direct ownership through private keys

Monetary neutrality: The network operates independently from corporate or sovereign liability structures

This explains why institutions, corporations, and sovereign entities continue integrating Bitcoin into treasury and reserve discussions. The relationship looks asymmetrical: Bitcoin is not integrating into the traditional system so much as the traditional system builds products around Bitcoin exposure.

Bitcoin Risks:

Adoption volatility: Price discovery remains aggressive as the network monetizes globally in real time

Operational responsibility: Self-custody transfers asset protection directly to the holder, requiring robust key management and operational security

Regulatory fragmentation: Jurisdictional treatment continues evolving unevenly across global markets

Layered scaling expansion: Throughput scales through secondary layers such as Lightning, Ark, and Fedimint rather than base-layer expansion

The volatility reflects monetary repricing rather than purely speculative behavior. As adoption expands, Bitcoin continues transitioning from a niche digital asset toward institutional collateral and sovereign reserve infrastructure.

TradFi vs CeFi vs DeFi vs Bitcoin: Why the Lines Are Blurring in 2026

The largest financial trend in 2026 is convergence between financial systems.

TradFi adopts blockchain settlement. CeFi integrates institutional compliance. DeFi expands into real-world assets.

Examples already visible by rail:

TradFi: Tokenized treasuries, bank-issued blockchain settlement infrastructure, Bitcoin ETFs, TradFi reaching toward Bitcoin, not Bitcoin changing to meet it

CeFi: Stablecoin settlement rails, regulated custody frameworks, institutional onboarding infrastructure

DeFi: On-chain money market funds, tokenized collateral systems, real-world asset protocols

Bitcoin remains structurally outside this convergence because the network has not changed and the rest of the financial stack is converging toward it. Unlike every other layer in the stack, Bitcoin holdings in self-custody cannot be frozen, seized, or deplatformed. A property that becomes more significant, not less, as institutional coordination over the other three rails deepens.

Convergence Trends:

TradFi: Adopting blockchain infrastructure to improve settlement efficiency

CeFi: Integrating institutional compliance and regulated custody systems

DeFi: Expanding into treasury products and real-world asset infrastructure

Bitcoin: Functioning as reserve collateral and decentralized settlement infrastructure

Three systems converge around financial coordination. Bitcoin remains externally anchored around monetary neutrality, an asset operating outside the system. That distinction may become more important as sovereign debt, tokenized assets, and stablecoin infrastructure expand globally.

Conclusion

TradFi, CeFi, and DeFi operate as competing financial architectures solving coordination, liquidity, compliance, and settlement problems across the same expanding digital capital environment.

Bitcoin operates differently.

Banks can tokenize assets. Exchanges can integrate stablecoin settlement. DeFi protocols can restructure lending, collateral, and yield markets through programmable infrastructure. Those systems increasingly overlap as blockchain settlement expands deeper into global finance.

Bitcoin's role remains narrower and more difficult to replicate: decentralized monetary settlement, fixed supply, self-custody, and neutrality outside institutional liability structures.

The result is not four equal systems merging into one unified framework. It is three financial architectures building around a separate monetary network already being pulled into the global capital stack.

FAQ

How do TradFi, CeFi, DeFi, and Bitcoin fundamentally differ from each other?

TradFi coordinates institutional finance through banks, brokers, regulators, and payment networks. CeFi uses centralized crypto platforms to simplify access to digital assets and connect fiat to crypto markets. DeFi replaces intermediaries with smart contract protocols that execute financial logic directly on blockchains. Bitcoin functions as a decentralized monetary network focused on fixed supply, settlement, and self-custody rather than broader financial coordination.

What are the main strengths and risks of Traditional Finance (TradFi)?

TradFi’s strengths include regulatory coordination, deep liquidity, consumer protection, and institutional credibility, producing predictability for large institutions. Its risks include slower settlement infrastructure, restricted global access, monetary expansion tied to central bank policy, and friction when integrating with blockchain-native systems.

Why is CeFi described as the bridge between banking and crypto, and what risks does it face?

CeFi is a bridge because centralized exchanges provide simplified user experiences, fiat connectivity, aggregated liquidity, and institutional access, so most capital enters crypto through them before DeFi. Its risks are counterparty exposure, custodial vulnerability, regulatory dependence, and liquidity contagion, as shown by collapses like FTX, Celsius, BlockFi, and Genesis.

In what way does Bitcoin operate differently from TradFi, CeFi, and DeFi, especially amid the convergence of financial systems?

TradFi, CeFi, and DeFi are converging around financial coordination through tokenization, stablecoins, compliance, and real-world asset integration. Bitcoin remains separate by coordinating monetary settlement with a fixed 21 million coin supply, decentralized settlement, self-custody, and neutrality outside institutional liability structures. Bitcoin holdings in self-custody cannot be frozen, seized, or deplatformed, and other systems are building products around Bitcoin rather than changing Bitcoin itself.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.