Quick summary

Bitcoin ownership is concentrating into mid-institutional 100–1,000 BTC wallets, shrinking retail

Total addresses hit record highs, driven mainly by many new sub-0.1 BTC holders

On-chain activity is at bear-market levels while price is high, reflecting off-chain ETF demand

A record 33% of supply is dormant 5+ years, while >100 BTC cohort hits all-time highs

Bitcoin address distribution in 2026 looks different from past cycles. More coins now sit in larger wallets, while mid-sized holders are shrinking. In earlier cycles, ownership spread outward during price rallies. In 2026, ownership is concentrating instead.

This article breakdown shows what each wallet group is doing now compared to 2017 and 2021, and what that says about who is buying and who is stepping back.

Bitcoin Address Distribution 2026 (Simple Breakdown)

A quick snapshot of who's holding what, and which direction each group is moving.

Small wallets (<0.1 BTC): Growing, new participants are entering at the smallest size

Mid wallets (0.1–1 BTC): Shrinking, fewer holders are maintaining mid-sized positions

Wholecoiners (1–10 BTC): Shrinking, whole-coin holders are losing whole-coin status

Larger holders (10–100 BTC): Stagnant no new growth in nearly seven years

Mid-institutional (100–1,000 BTC): Expanding to all-time highs, the clearest growth signal in the data

Super-whales (>1,000 BTC): Flat, still below their 2021 peak.

What the above means: Bitcoin ownership is concentrating into mid-institutional addresses, while the retail middle layer is being hollowed out. The bottom and top of the distribution are moving in opposite directions.

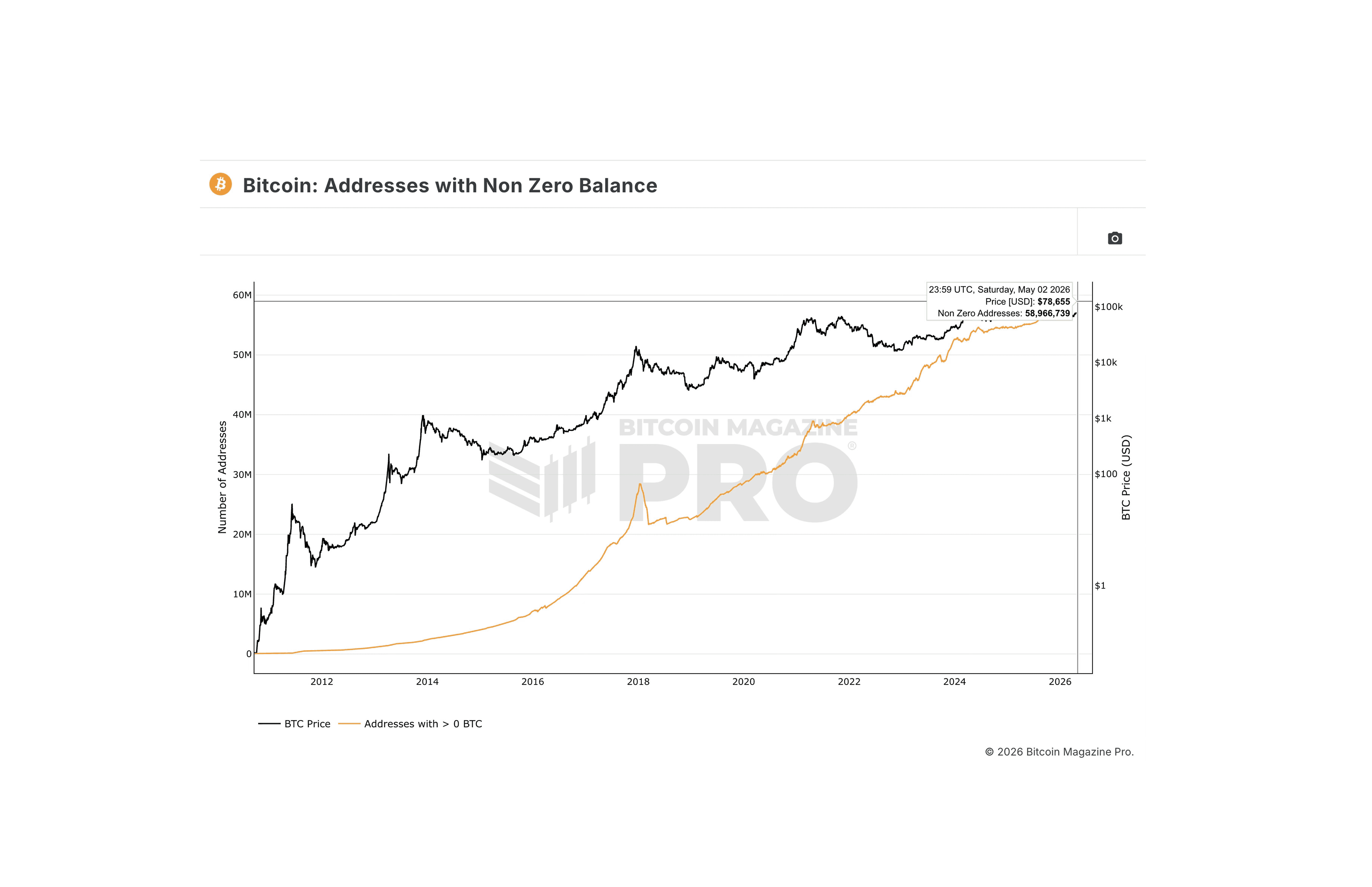

Total Wallets: More Holders Than Ever

The total number of Bitcoin addresses holding any amount of BTC reached 58,966,739 on May 2, 2026, an all-time high. In January 2018, near the last cycle's retail peak, that number was 28,385,652.

The total holder base has doubled in eight years.

Total wallets continue to rise, but most of that growth is coming from very small balances. Roughly 4.7 million new addresses have been added below the 0.1 BTC threshold since mid-2024. Compared to past cycles, new entrants are committing less capital per address, likely a mix of stats-stackers, exchange withdrawal addresses, and Lightning users.

Mid-Sized Holders Are Shrinking

Three retail-adjacent cohorts have been losing addresses since their respective peaks. This is the first cycle in Bitcoin's history where multiple holder bands are contracting at the same time price climbs.

Cohort changes from peak:

>0.1 BTC: Peaked October 2024 at 4,580,538. Currently 4,488,423. Down ~92,000.

>1 BTC (wholecoiners): Peaked October 2023 at 1,021,893. Currently 975,445. Down ~46,000.

>10 BTC: Peaked September 2019 at 157,276. Currently 150,476. Down ~7,000 and has not made a new high in nearly seven years.

What this means: In 2017 and 2021, every one of these cohorts grew into the price top. New buyers crossed the 1 BTC and 10 BTC thresholds during bull markets. This cycle, the threshold is being crossed downward where wholecoiners are losing whole-coin status as they sell, consolidate, or move funds into ETF custody.

The middle layer of Bitcoin ownership is thinning. Fewer holders are maintaining meaningful positions.

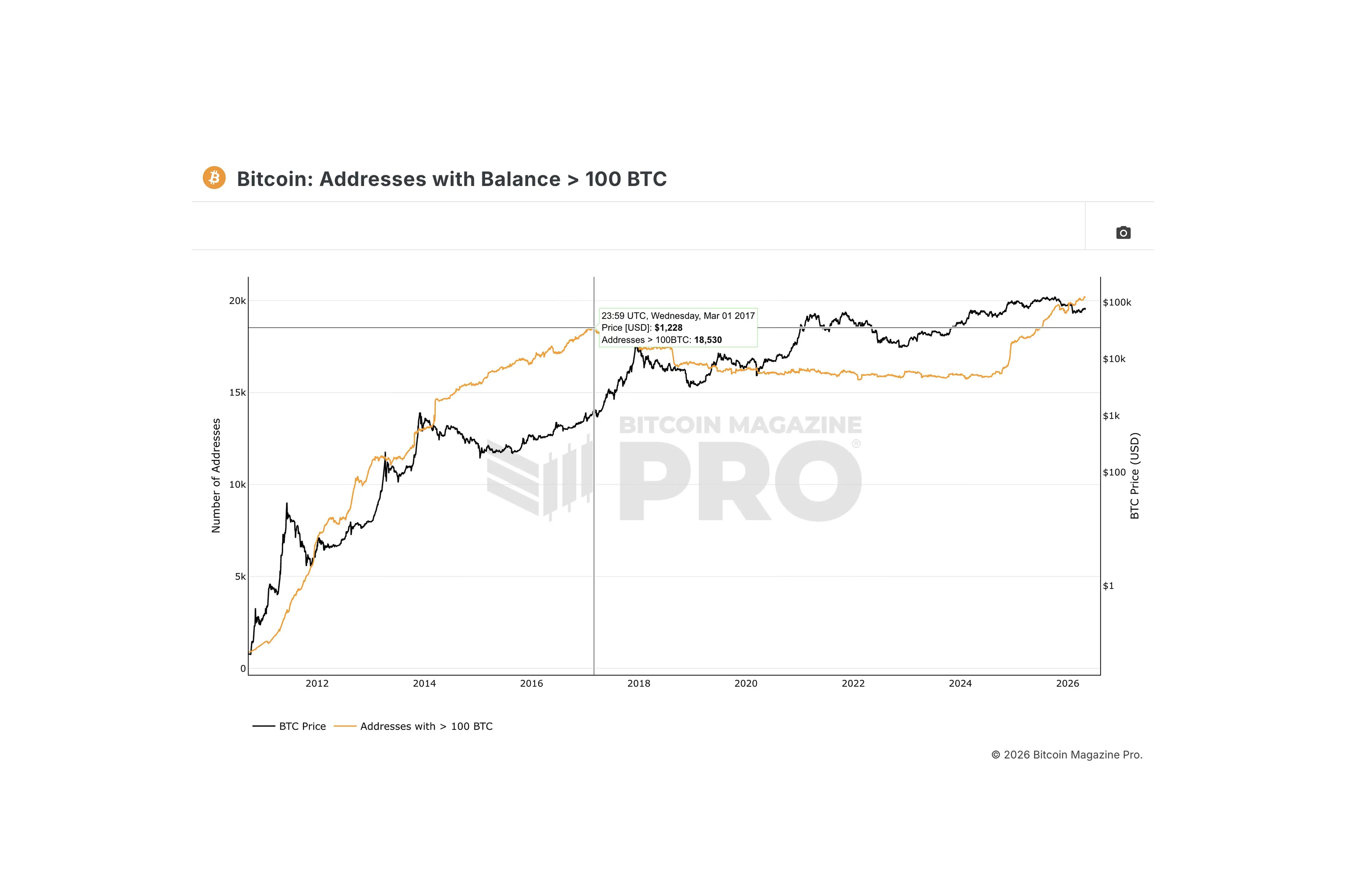

The Mega-Whale Cohort Just Broke an 8-Year Range

The cleanest growth signal in the data comes from the >100 BTC cohort. This group sat between roughly 16,000 and 18,500 addresses for nearly a decade, through the 2017 top, the 2018 bear, the 2021 top, and most of 2024.

The breakout in numbers:

March 2014: 14,529 addresses (price $636)

December 2017 cycle top: 17,557 (price $14,081)

June 2019 floor: 16,176 (price $9,285)

October 2024: 16,024 (price $62,103) still in the same range

July 2025 breakout: 18,582 (price $108,953) range broken

May 2026: 20,204 (price $78,655) all-time high

What this means: For nine years this >100 BTC cohort cohort never sustainably crossed 19,000. In mid-2025 it broke out, and it has kept climbing. Mid-institutional addresses, the size class consistent with corporate treasury allocations, ETF custody sub-accounts, and large fund cold storage are being created at a pace not seen in Bitcoin's history.

Compared to past cycles: In 2017 and 2021, this same cohort was flat or declining near price tops as early holders distributed to retail. This cycle, it is doing the opposite. Whoever is filling these addresses is buying at all-time highs and not selling.

This is the clearest difference between this cycle and past ones: large holders are expanding while retail activity remains muted.

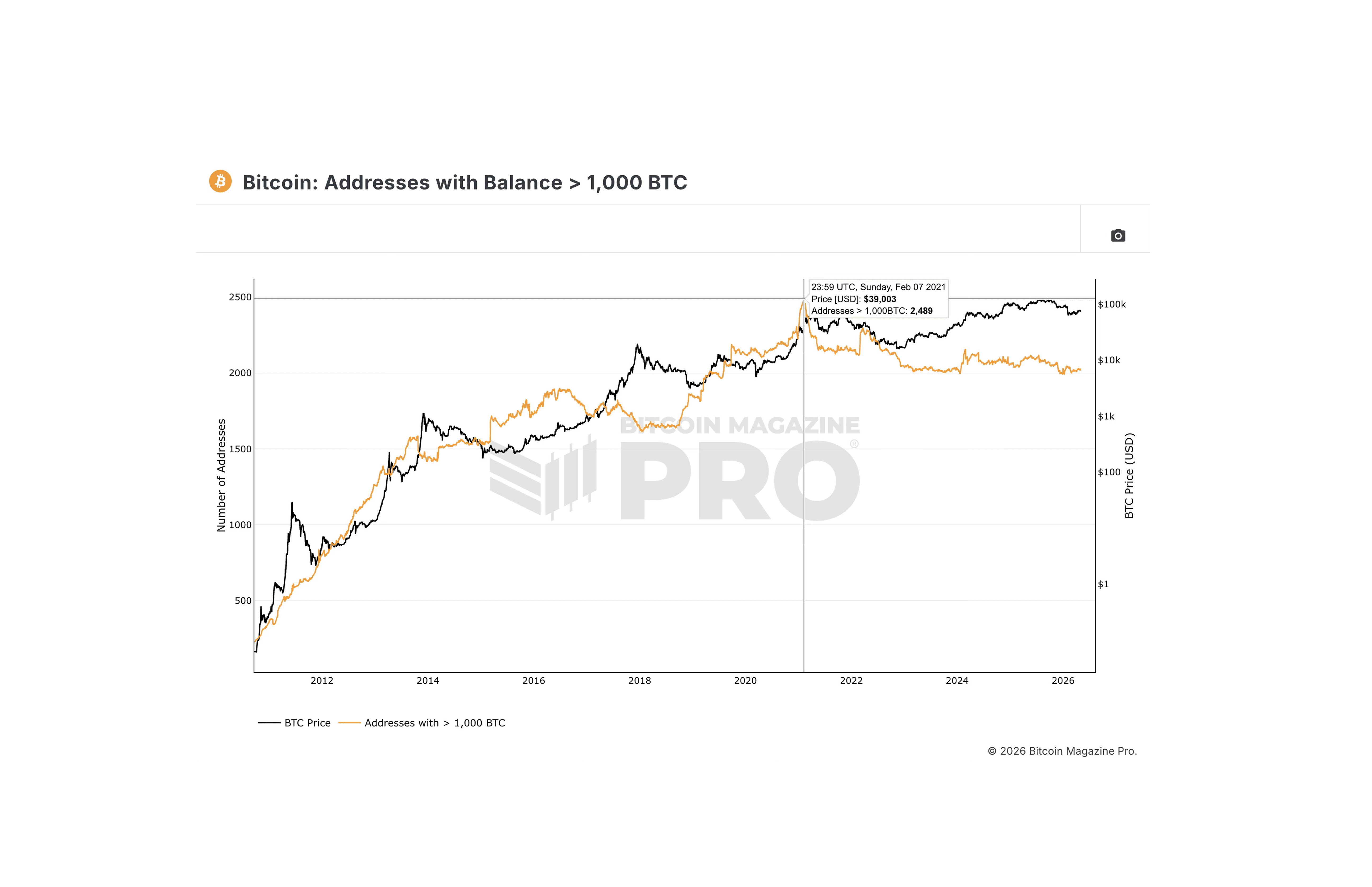

The Super-Whale Cohort Tells a Different Story

The >1,000 BTC cohort — the very largest holders — has not joined the breakout.

Feb 2021 peak: 2,489 addresses (price $39,003)

Feb 2023: 2,013 (price $23,146)

April 2026: 2,020 (price $76,345)

Reading the gap: The super-whale tier is sitting roughly 19% below its February 2021 peak. While the >100 BTC cohort prints fresh ATHs, the >1,000 BTC cohort has gone nowhere for three years.

What this means: Institutional custody (Coinbase Custody, Fidelity, BitGo, ETF cold storage) holdings span across many sub-1,000 BTC addresses for operational and security reasons rather than concentrating into mega-wallets. Institutional flows show up in the 100–1,000 BTC tier, not above it. The flat super-whale count is not "no big money buying" — it just means the fingerprint of institutional buying lives one tier lower than it did in 2021.

We know this because ETF and custodian disclosures show holdings well above 1,000 BTC, but those balances are deliberately split across many smaller addresses for security and audit reasons. The supply is there, it just doesn't show up in one big wallet.

On-Chain Activity Is at Bear-Market Lows While Price Is 35% Below ATH

Activity is low compared to past cycles even though price is around the highs. Even at 35% off the all-time high, $78K is a price Bitcoin only reached for the first time in late 2024, historically, this is a bull-cycle level, not a bear-cycle one. In earlier cycles, activity increased with price. That is not happening now.

Active addresses (7-day moving average):

December 2016 (pre-bull base): 642,897 at $891

February 2019 (post-bear floor): 642,900 at $3,411

November 2022 (FTX crisis): 982,750 at $16,856

May 2026: 636,019 at $78,172

What this means: Daily Bitcoin on-chain activity is at the same level seen during deep bear-market lows in 2016 and 2019. The metric peaked at ~1.2M in 2017 and ~1.25M in 2021, and has never reclaimed 1M during the entire 2024–26 bull run.

Activity appears low because a growing share of demand is happening off-chain, through ETFs and custodial systems that do not register on the blockchain.

Old Coins Are Sitting Stiller Than Ever

A record share of Bitcoin's supply has not moved in years.

Supply locked by age (May 2026):

5+ years dormant: 33.14% an all-time high. Roughly 6.5 million BTC has not been touched since at least May 2021.

1+ year dormant: 60.13%, down from a December 2023 peak of 70.69%.

Comparison to past cycle tops:

2018 top: 5+ year HODL was ~17%

2021 top: 5+ year HODL was ~22%

2026 ($78K+): 33.14%

What this means: In 2017 and 2021, old coins woke up as price climbed, long-term holders distributed to new buyers, and the metric dropped. That was the classic top signature. None of that is happening now. The opposite is happening: long-term supply keeps growing as a share of total bitcoin in circulation.

The 1+ year caveat: The 1+ year band has come down from 70.69% (Dec 2023) to 60.13% (May 2026). Old coins are moving just slowly, into rising prices. This is the most cycle-typical signal in the dataset and suggests the bull cycle is mid-to-late stage, but the magnitude is well below 2017 or 2021.

Bitcoin Past Cycles vs Now

A side-by-side comparison anchors the difference.

At the 2017 cycle top ($20K, December 2017):

Active addresses were near 1.2M, freshly making all-time highs

Wholecoiner cohorts (>1, >10, >100 BTC) declining as early holders distributed

5+ year HODL near 17%

At the 2021 cycle top ($69K, November 2021):

Active addresses near 1.25M

Wholecoiner cohorts peaking near top

5+ year HODL near 22%

Today ($78K, May 2026):

Active addresses at 636,019, a deep bear-market reading

Mid-retail and wholecoiner cohorts (>0.1, >1, >10 BTC) all declining from peak

The >100 BTC cohort breaking out to a new all-time high

5+ year HODL at all-time high (33.14%)

The fingerprint is inverted from 2017 and 2021. The metrics that historically marked tops are not generating top signals and the metric that's growing fastest (mid-institutional address count) historically grew during accumulation phases, not at price ATHs.

What This Means for Readers

Coins are moving from many retail wallets into fewer, larger institutional wallets and once they get there, they stop moving.

Tiny holders are still arriving: Sub-0.1 BTC addresses keep growing

Mid-sized retail holders are leaving: Anyone who used to hold 0.1 to 10 BTC is being slowly thinned

Mid-institutional addresses are exploding: The 100–1,000 BTC tier is at all-time highs. Corporate treasuries, ETF custody, and fund cold storage live here

Super-whales are flat: Institutional flows fragment below the 1,000 BTC threshold

Old coins are not moving: A record one-third of all bitcoin has sat still for five-plus years

On-chain activity is quiet: Demand is being settled off-chain.

The metrics that called every previous cycle top are silent because the marginal buyer is no longer retail.

Readers interested in deeper structural analysis can explore the framework outlined in the Coinjuice ebook.

Conclusion

Bitcoin ownership is more concentrated than in past cycles. Retail cohorts are contracting, mid-institutional cohorts are at all-time highs, and a record share of supply has been locked in cold storage for five-plus years.

The key things to watch now are whether long-term holders begin selling, visible in the 1+ year HODL wave, currently 60.13% and whether the >100 BTC cohort continues to grow. A continued decline in the HODL wave would suggest classic late-cycle distribution. A bounce higher would suggest accumulation is reasserting itself.

Analysis based on 30+ on-chain charts across wallet cohorts, activity metrics, and HODL data. Source: Bitcoin Magazine Pro. Snapshot: May 2, 2026.

FAQ

How has Bitcoin address distribution changed in 2026 compared to past cycles?

In 2026, ownership is concentrating into larger, mid-institutional wallets while mid-sized retail holders are shrinking. Small wallets under 0.1 BTC are growing, mid wallets (0.1–1 BTC) and wholecoiners (1–10 BTC) are shrinking, 10–100 BTC wallets are stagnant, 100–1,000 BTC wallets are expanding to all-time highs, and >1,000 BTC super-whale wallets are flat and below their 2021 peak.

What is happening to total Bitcoin wallet counts and where is the growth coming from?

Total Bitcoin addresses holding any amount of BTC reached an all-time high of 58,966,739 on May 2, 2026, about double the count from January 2018. Most of the recent growth comes from very small balances, with roughly 4.7 million new addresses added below the 0.1 BTC threshold since mid-2024.

Why is the >100 BTC cohort significant in this cycle?

The >100 BTC cohort has broken out of a 9-year range of roughly 16,000–18,500 addresses and reached an all-time high of 20,204 in May 2026. This tier, associated with corporate treasuries, ETF custody sub-accounts, and large fund cold storage, is expanding while price is high, indicating large holders are buying at all-time highs and not selling, unlike in past cycles.

How do current on-chain activity and HODL patterns compare with previous cycle tops?

Active addresses are around 636,019 in May 2026, a level similar to deep bear-market lows and far below the ~1.2–1.25 million seen near the 2017 and 2021 tops. At the same time, a record 33.14% of supply has been dormant for 5+ years, much higher than ~17% in 2018 and ~22% in 2021, while 1+ year dormant supply has eased from 70.69% to 60.13%, suggesting a mid-to-late stage bull cycle with slower long-term holder distribution than in past tops.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

More like this

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.