Quick summary

Article defines five strict Ponzi criteria and reviews major historical Ponzi schemes

Traditional finance relies on confidence and inflows but is not classified as Ponzi fraud

Bitcoin lacks a central operator, opaque accounts, guaranteed returns, and unsustainable liabilities

On-chain transparency, fixed supply, and long-term holder behavior contradict core Ponzi scheme dynamics

Bitcoin has been called a Ponzi scheme by economists, journalists, and financial commentators for fifteen years plus. The “Ponzi” label carries emotional weight, but it also describes a historically specific fraud structure that should be applied carefully and precisely.

Traditional Ponzi structures depend on centralized operators, hidden liabilities, fabricated returns, and continuous redistribution from newer participants to earlier ones. Bitcoin operates through a transparent issuance schedule, open settlement layer, and voluntary market pricing, making the comparison more complex than the headline suggests. Examining the differences directly helps clarify where the analogy holds, where it breaks down, and why it continues to persist.

What Is a Ponzi Scheme?

The definition must be precise before any comparison holds.

A Ponzi scheme has five structural features:

Central operator controls the asset pool: A human holds the money and can lie about it, move it, or disappear with it.

Early investors paid from new capital: No productive activity generates returns. Money circulates from new entrants to old ones.

Collapse is structurally inevitable: When inflows slow, the scheme fails immediately. There is no floor and no surviving asset.

Opacity is the mechanism: The fraud works only because investors cannot verify the truth. Transparency kills it instantly.

Promises exceed reality: Returns are guaranteed, fabricated, or both.

Four of these characteristics are drawn from SEC investor guidance. The fifth — structural inevitability of collapse — is the logical conclusion of the model the SEC describes.

Every scheme in the last hundred years has carried all five features. These five points are the checklist.

Famous Ponzi Schemes From the Last 100 Years

The scale changed, but the underlying structure remained consistent. SEC, DOJ, FBI, court, and on-chain records show the same pattern across cases: promised returns, opaque accounting, dependence on new inflows, and eventual collapse.

Charles Ponzi | 1920 | $20M: Promised returns on postal arbitrage that never existed. Collapsed within months when press scrutiny triggered withdrawals.

MMM Russia | 1994 | ~$10B: Pure recruitment pyramid with no underlying asset. Defrauded over 10 million people. Collapsed when inflows dried up.

Greater Ministries International | 1996–1999 | $500M: Affinity fraud targeting church communities. Bible verses used to solicit retirement funds. Shut down by the FBI.

Madoff Securities | 1991–2008 | ~$50B: Fabricated trading statements for nearly two decades. Collapsed during the 2008 redemption surge when withdrawal demands exceeded available cash.

Stanford International Bank | 2000s | $8B: Fake certificates of deposit promising above-market returns. Brought down by SEC investigation.

Bitconnect | 2016–2018 | ~$2B: Promised returns from a proprietary trading bot that did not exist. Collapsed under simultaneous regulatory pressure across multiple jurisdictions.

OneCoin | 2014–2017 | ~$4B: Marketed as a cryptocurrency with no blockchain ever built. Founder Ruja Ignatova remains a fugitive. Victims largely unrecovered.

PlusToken | 2018–2019 | $3B: Crypto wallet exit scam. Traced and partially recovered through on-chain forensics.

According to PonziTracker, 60 alleged Ponzi schemes were uncovered in 2019, involving approximately $3.245 billion in investor funds.

How the Traditional Financial System Compares to Ponzi Structures

Before applying the checklist to Bitcoin, the traditional financial system deserves the same scrutiny. The comparison is about understanding how modern financial systems manage liquidity, obligations, and confidence under stress.

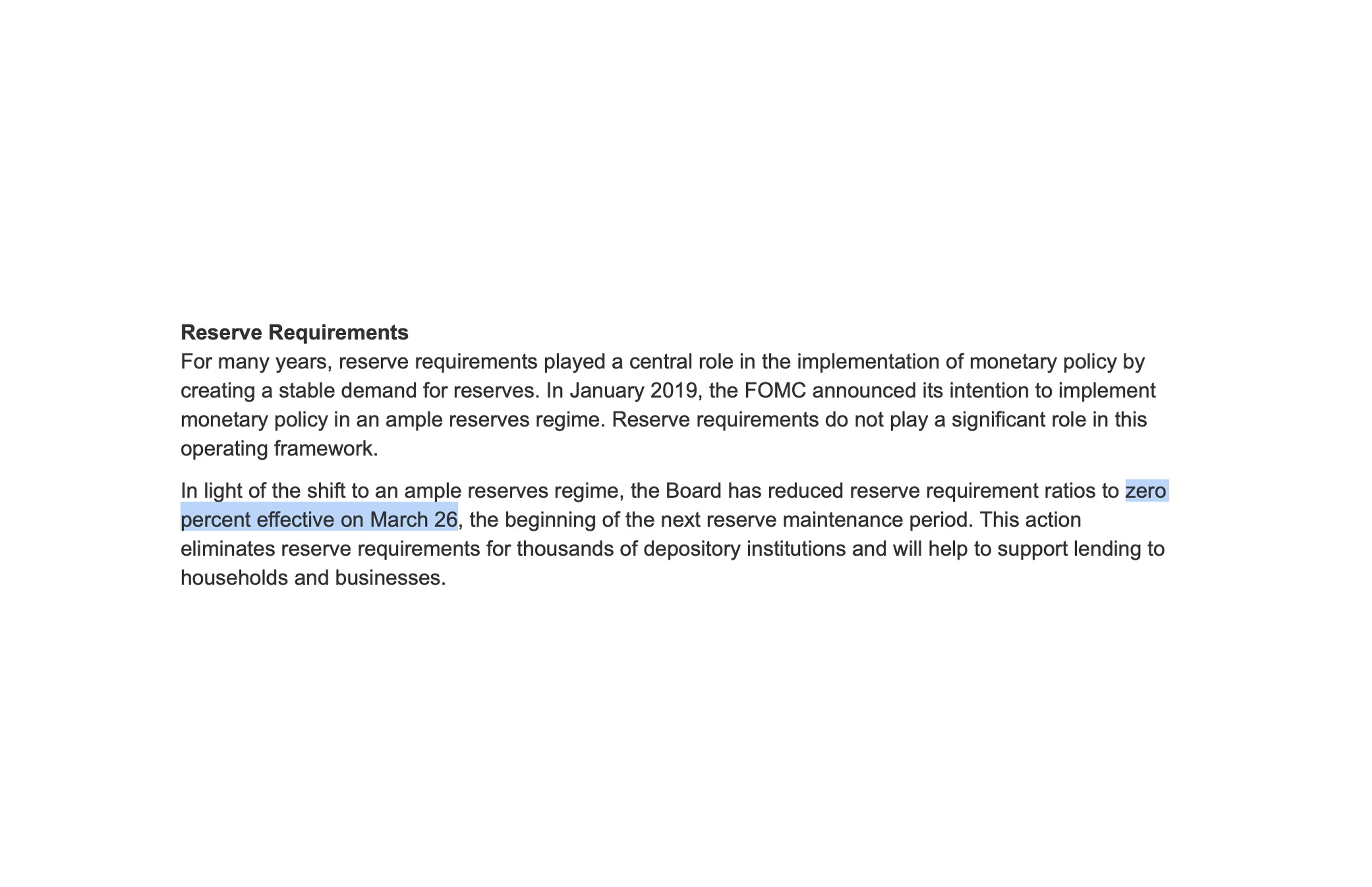

Zero reserve requirements: In 2020, the US Federal Reserve reduced reserve requirement ratios for American banks to zero percent. Banks are no longer required to hold a fixed percentage of customer deposits as reserves, although capital, liquidity, and stress-testing requirements still apply. Deposits are primarily supported by bank assets, liquidity management, institutional confidence, and FDIC insurance rather than one-to-one physical cash reserves

Insurance solvency dependency: Insurance systems operate by pooling premiums from many policyholders to cover claims from the few. These models rely on actuarial assumptions, reserve management, and liquidity planning. During periods of widespread simultaneous claims or financial stress, the capital supporting those liabilities can come under pressure relative to simultaneous claims.

Perpetual debt rollover: US government national debt is largely rolled forward through new bond issuance rather than repaid through sustained fiscal surplus. Maturing debt is routinely refinanced, while the debt-to-GDP ratio has continued rising over time.

None of this constitutes a Ponzi scheme. These systems generate real economic activity, operate under legal regulation, and involve disclosed risk. The distinction matters and should be maintained carefully.

Like all modern financial systems, stability depends on continued participation, liquidity, and confidence during periods of stress.

Is Bitcoin a Ponzi Scheme? Bitcoin vs Ponzi Scheme Characteristics

Does a central operator control the asset pool?

No. Bitcoin operates on a decentralised network of thousands of independent nodes and miners globally.

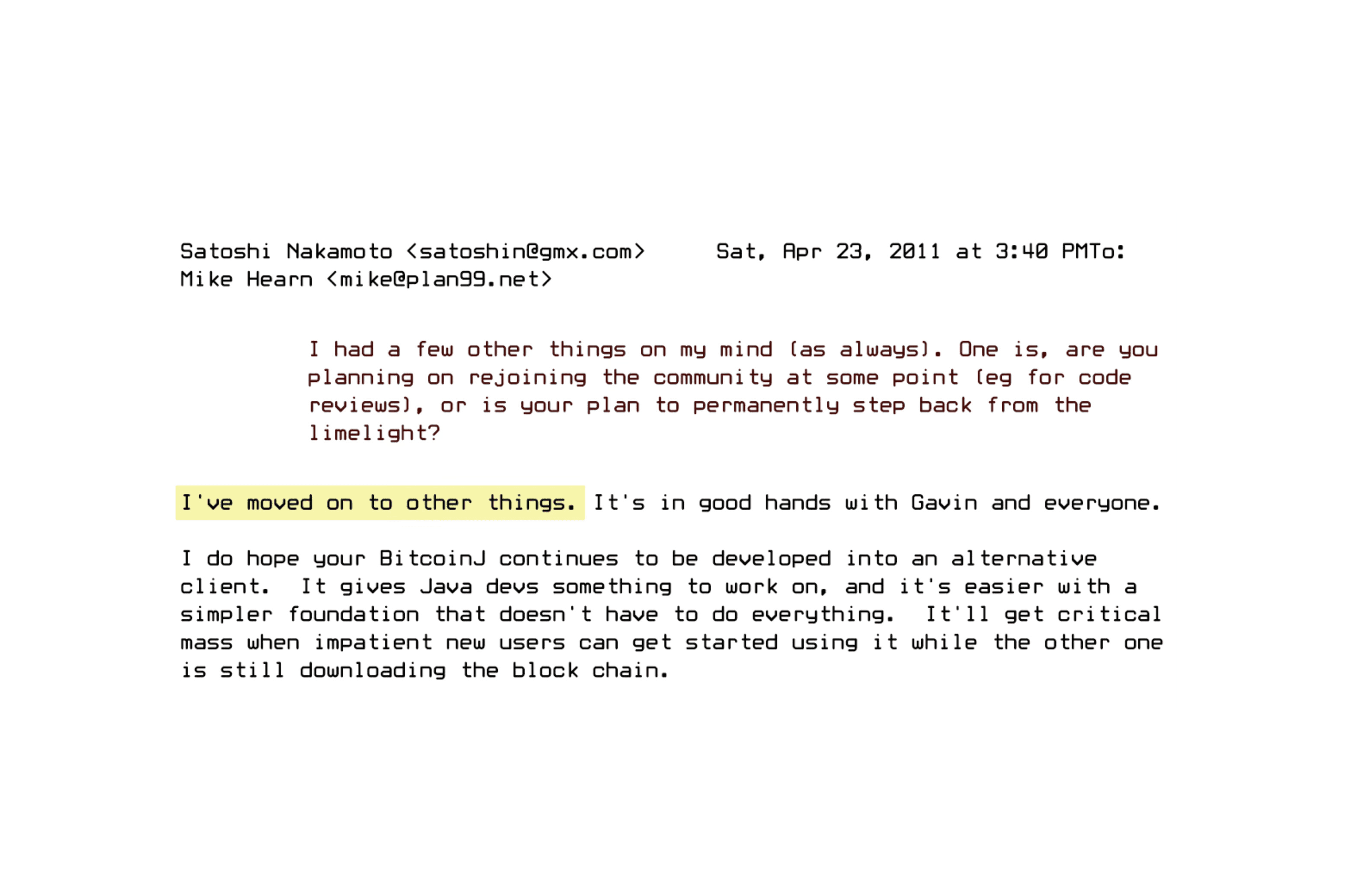

Satoshi Nakamoto has not publicly interacted with the protocol since 2011. No single entity can freeze funds, fabricate balances, or alter the supply schedule. The protocol enforces the rules. Humans do not.

The failures historically associated with Bitcoin — Mt. Gox, FTX — were not failures of the protocol. They were centralised custodians who misrepresented reserves. The Bitcoin public ledger was never compromised. The humans controlling custodial businesses were the problem, not the asset.

Do Early Bitcoin Holders Profit From New Buyers?

This is the strongest version of the Bitcoin Ponzi argument and deserves a direct answer.

Observation: Early Bitcoin holders benefit most when adoption and demand increase over time

Relevant comparison: The same dynamic exists in gold, land, fine art, scarce assets with limited supply, and real estate purchased before major price appreciation

Key distinction: Appreciation driven by rising demand is market price discovery, not fraud. Bitcoin carried substantially more uncertainty when it traded below $100,000 and had not yet reached broader institutional adoption.

That dynamic is further complicated by Bitcoin's four-year cycle structure. Entry price matters more than entry date.

A buyer at the 2013 cycle top at $1,000 underperformed a buyer who entered in 2016 at $600. A buyer at the 2021 cycle top at $69,000 remains underwater against buyers who entered in 2023 at $25,000. In a Ponzi scheme, chronological order determines outcome. In Bitcoin, market timing and cycle position determines outcome. Those are structurally different things.

A framework for identifying those entry points is outlined in the Coinjuice no-leverage trading guide.

Since the Bitcoin white paper was published in 2008, no operator has manufactured returns, guaranteed yield, or created liabilities within the protocol itself. The market determined outcomes. The protocol did not.

Does Bitcoin Eventually Collapse Like a Ponzi Scheme?

A Ponzi scheme must collapse. When inflows stop, liabilities exceed reserves immediately because the reserves were never real.

No productive asset exists beneath the structure.

Bitcoin operates on a different foundation:

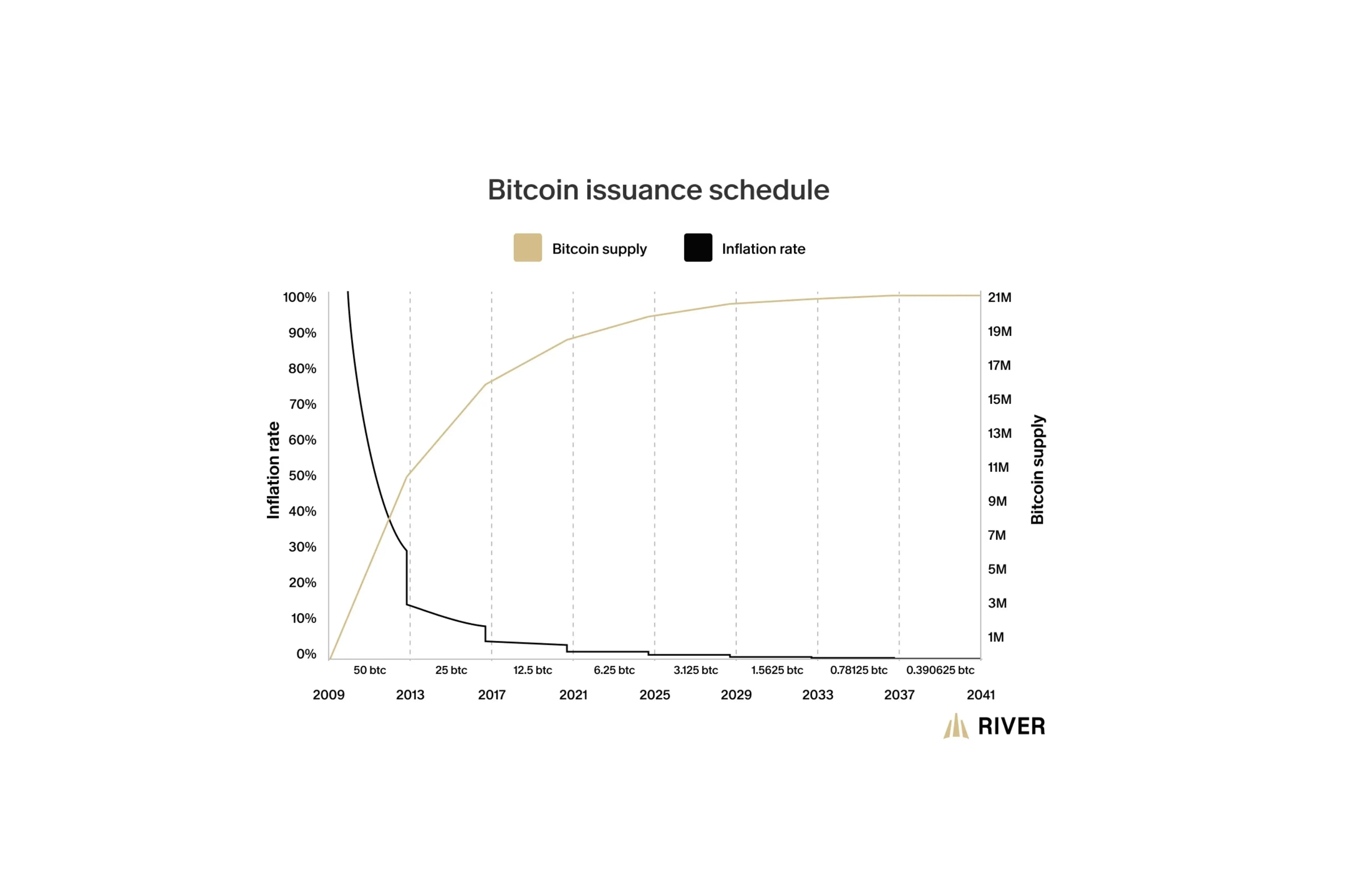

Fixed supply: 21 million coins, mathematically enforced at the protocol level. No operator can change the fixed supply

Public verification: Supply and every transaction are auditable in real time through any block explorer. No filing. No auditor. No intermediary required

No structural expiry: Price can fall. Demand can collapse. Volatility can persist. The protocol continues operating regardless because there is no mechanism within Bitcoin itself that forces insolvency or shutdown. Even in a scenario involving large-scale internet disruption, the network would become temporarily inaccessible rather than structurally invalid, resuming normal operation once connectivity returned.

A deeper breakdown of Bitcoin’s behaviour during internet outages is explored here. A demand collapse is market risk. Structural fraud requires something else entirely: an operator who controls the pool, fabricated reserves, and liabilities that were never backed by anything real.

Bitcoin Transparency vs Ponzi Scheme Opacity: Why the Comparison Fails

Ponzi schemes are structurally dependent on opacity. Which means the fraud only functions because investors cannot verify what is actually happening inside the structure. The moment full transparency is introduced, the scheme collapses instantly because the gap between what is promised and what actually exists becomes visible to everyone simultaneously.

The fraud holds only as long as investors cannot verify what is actually happening.

Transparency kills it. Systems built around real-time audibility and publicly verifiable reserves operate very differently from structures dependent on delayed reporting and opaque balance sheets.

Bitcoin is the opposite:

Full transaction history is public: Every transaction ever processed on the network is openly verifiable by anyone

Supply updates in real time: The circulating supply figure requires no quarterly report, no trusted auditor, and no operator disclosure

Verification is trustless: Confirmation happens directly through the network. No intermediary needs to be believed.

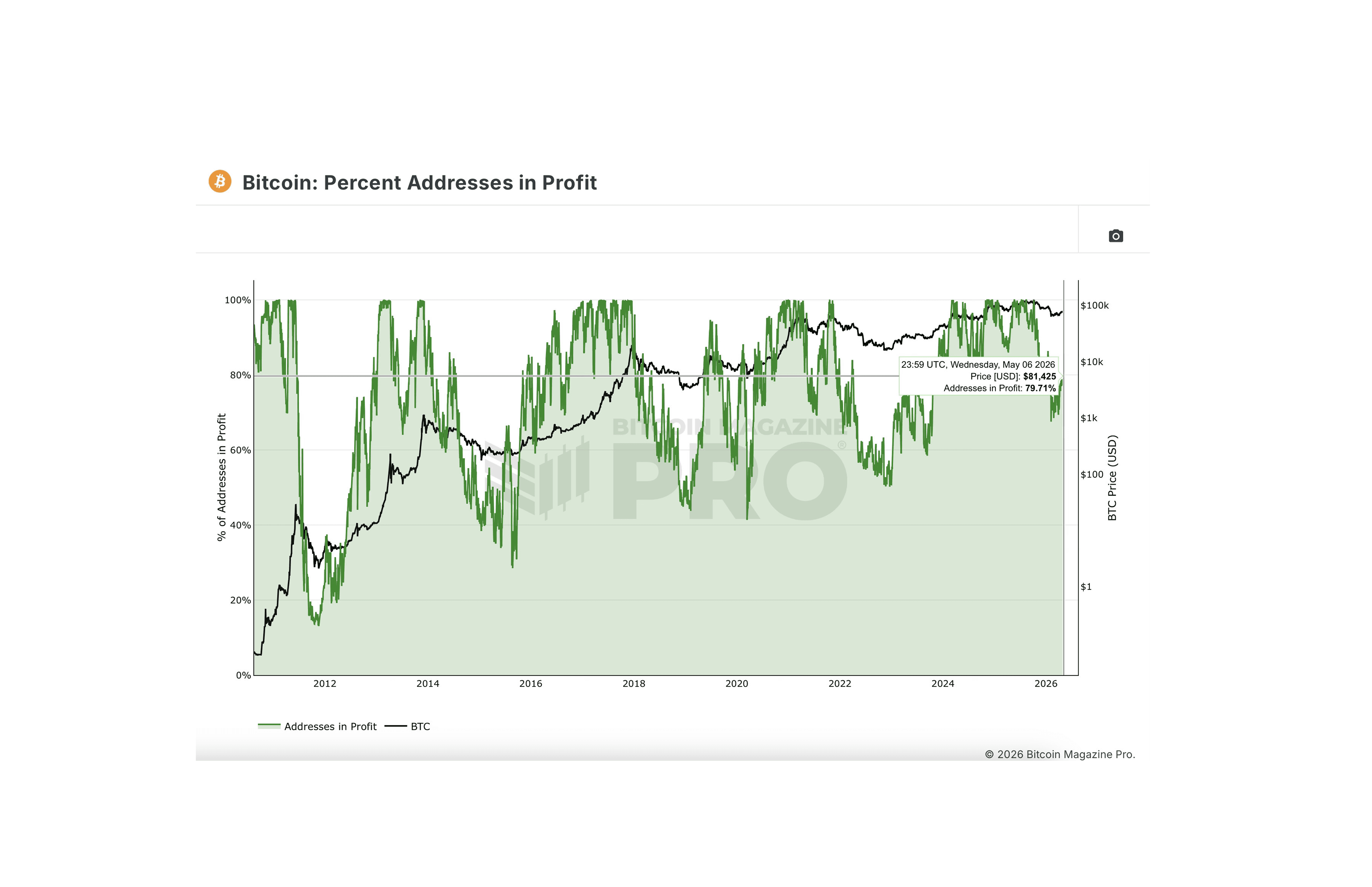

According to on-chain BitcoinMagazine Pro, approximately 80% of Bitcoin addresses were in profit as of May 6, 2026 at a price of $81,000.

Unlike a Ponzi scheme — where profitability figures are fabricated and unverifiable — that number is auditable directly through the ledger in real time.

Does Bitcoin Create Financial Liabilities?

This is the cleanest structural distinction in the entire comparison in this research piece.

Ponzi schemes create liabilities they cannot ultimately satisfy:

Promised returns: Investors are told what they will earn

Redemption obligations: Capital is expected to be repayable

Fabricated yields: Returns are funded through new inflows rather than productive activity

Contractual payout expectations: The operator owes liabilities to participants.

Bitcoin creates none of the above liabilities:

No guaranteed yield: The protocol makes no return promise

No redemption promise: There is no operator to redeem from

No maturity date: The asset does not expire

No balance sheet claim: Holding Bitcoin is not a contractual relationship.

Ownership of Bitcoin is possession of a bearer asset with a fixed, publicly verifiable supply. Nothing is owed. Nothing is promised. The protocol continues operating regardless of price.

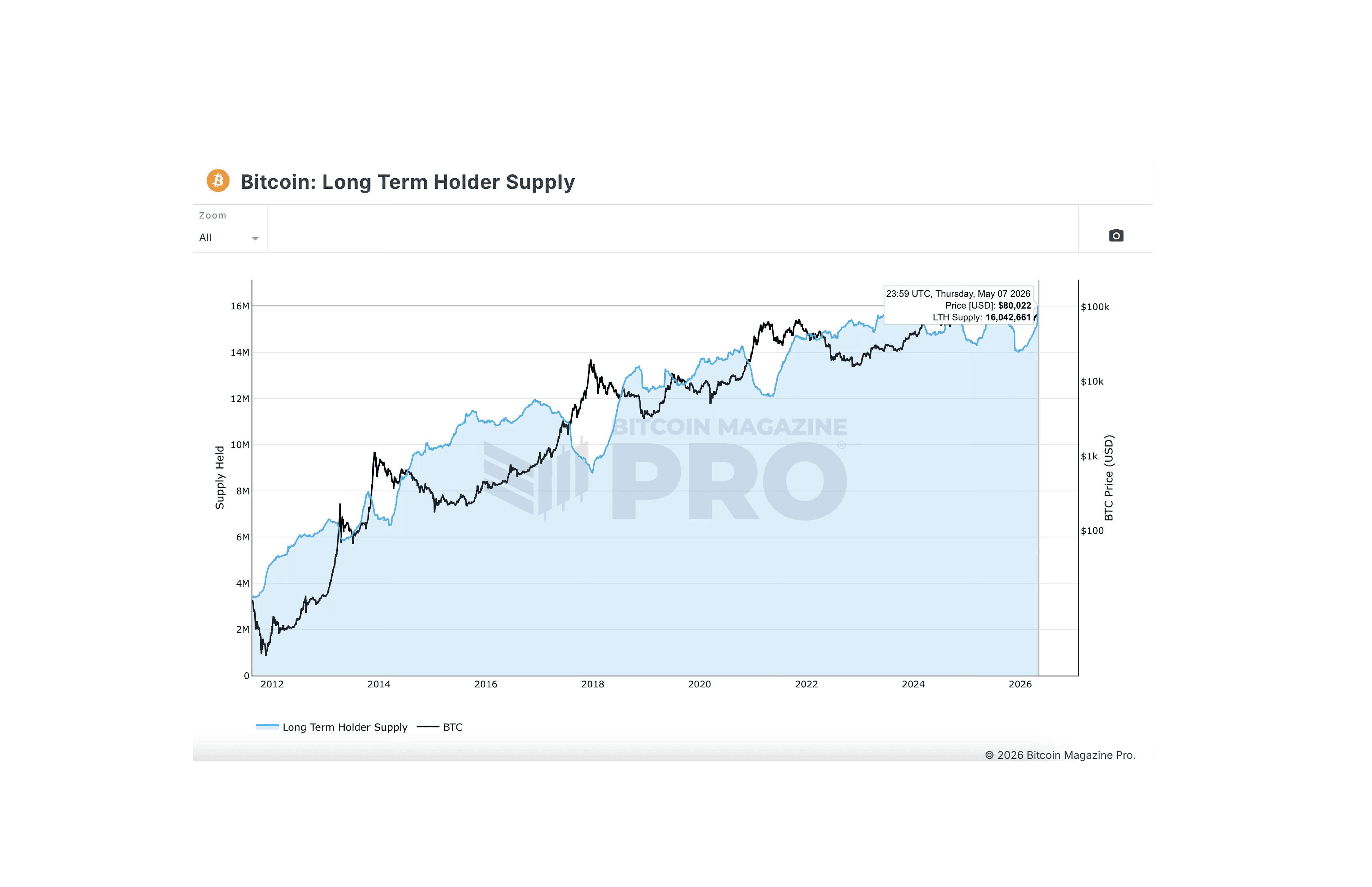

Bitcoin Long-Term Holder Data To Watch

The percentage of supply held by long-term holders wallets unmoved for more than one year is one of the most reliable on-chain indicators of where Bitcoin is in its adoption cycle.

Rising long-term holder supply during corrections: Accumulation is occurring. Holders are absorbing sell pressure rather than capitulating to it

Falling long-term holder supply during rallies: Distribution is underway. Early holders are rotating into liquidity as new buyers enter.

At $80,022, long-term holder supply has climbed back toward 16 million BTC approaching the prior all-time high in conviction-wallet supply set in 2023. Price pulled back from $100k and long-term holders did not sell. That is the accumulation pattern in real time. In a Ponzi scheme, participants exit during corrections. The on-chain data from BitcoinMagazine Pro shows the opposite.

That behavioral pattern separates speculative trading activity from long-term monetary adoption and it is fully auditable on-chain in real time.

For a deeper framework on how Bitcoin's fixed supply creates compounding adoption pressure over time and why Bitcoin is the ultimate game theory trap.

Conclusion

Against five diagnostic criteria, Bitcoin fails the Ponzi test on every count except arguably on one: early holders benefit more than late holders during appreciation. As shown above, even that single overlap breaks down under cycle analysis.

Not fraud: No operator manufactured the return

Not structural: No mechanism inside the protocol forces collapse

Not inevitable: Demand risk is market risk. Those are different things.

The stronger critique of Bitcoin is not that it is a Ponzi. It is that the asset generates no cash flow and price depends entirely on continued demand, which raises a legitimate valuation debate that ties directly to Bitcoin's utility as a bearer asset that safeguards the holder from money debasement.

The banking system operates with zero reserve requirements. Insurance funds a fraction of total liability. Government debt rolls forward indefinitely. None of those facts make those systems Ponzi schemes. They do clarify that structural dependency on continued inflows is not unique to Bitcoin.

The accusation requires precision before it carries weight. With 80% of addresses in profit on May 7, 2026 in a bear market. 21 million coins. No operator. No promises. No liabilities. Open ledger.

The checklist has been run. Bitcoin is not a Ponzi.

FAQ

What are the five structural features of a Ponzi scheme?

A Ponzi scheme has five key features: a central operator controls the asset pool; early investors are paid from new capital with no productive activity generating returns; collapse is structurally inevitable when inflows slow; opacity prevents investors from verifying the truth; and promised returns are guaranteed, fabricated, or both.

Why does Bitcoin not meet the central-operator criterion of a Ponzi scheme?

Bitcoin runs on a decentralized network of thousands of independent nodes and miners, with no single entity able to freeze funds, fabricate balances, or change the supply schedule. The protocol enforces the rules, and historical failures like Mt. Gox and FTX were due to centralized custodians misrepresenting reserves, not the Bitcoin network itself.

How does Bitcoin’s transparency differ from the opacity of Ponzi schemes?

Ponzi schemes depend on opacity, collapsing once full transparency reveals the gap between promises and reality. Bitcoin is the opposite: every transaction is publicly verifiable, supply updates in real time without auditors or operator disclosures, and verification is trustless through the network. Profitability metrics, such as the share of addresses in profit, are auditable directly on-chain.

Does Bitcoin create financial liabilities like a Ponzi scheme?

No. Ponzi schemes create liabilities through promised returns, redemption obligations, fabricated yields, and contractual payout expectations. Bitcoin does not guarantee yield, offer redemption, have a maturity date, or represent a balance sheet claim. Holding Bitcoin is owning a bearer asset with a fixed, publicly verifiable supply, with no promises or obligations attached.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

More like this

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.