Quick summary

Most tokenised assets like BlackRock's BUIDL sit idle, revealing low DeFi infrastructure trust in 2026

Five-point audit focuses on real usage, protocol revenue, P/S ratios, and crisis performance

Framework distinguishes earned from rented liquidity by observing TVL behavior when incentives stop

Valid audits require recency, open-source code, battle testing, protecting capital in future crises

Most crypto projects look identical from the outside. They show big numbers. They post nice charts. They share audit stamps from companies most people have never heard of.

But the data tells a different story.

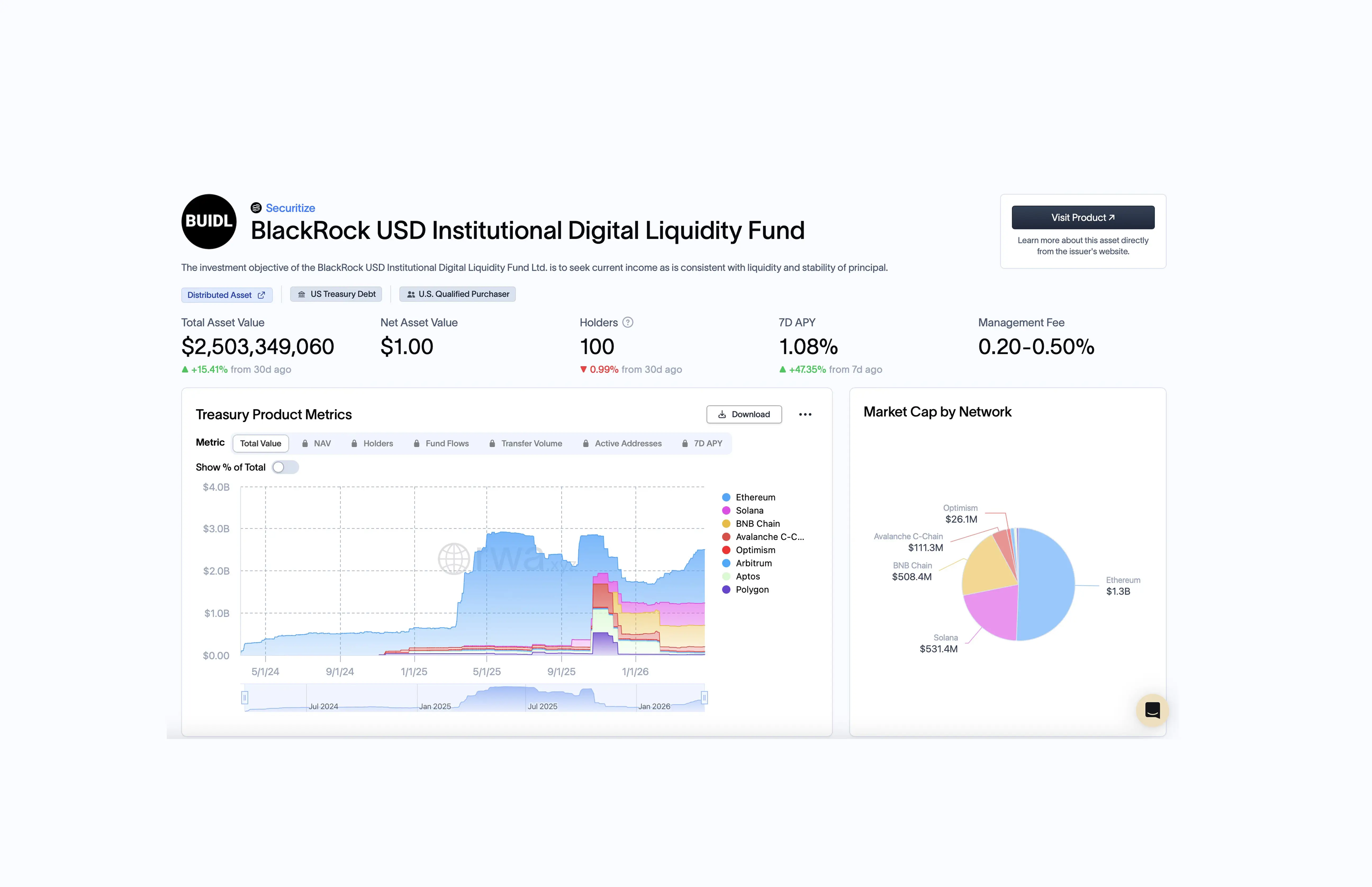

BlackRock's BUIDL fund is a tokenised money market vehicle backed by short-dated US Treasury bills, overnight repos, and cash. According to RWA.xyz, it holds $2.5 billion across eight blockchains as of April 27, 2026. According to DefiLlama, only $18.8 million of that — 0.75% — is actively deployed in DeFi protocols. The remaining $2.48 billion sits in wallets, collecting yield from US government debt while it waits for DeFi infrastructure it does not yet trust enough to use.

BlackRock is not the exception. It is the template. Most tokenised assets in 2026 follow the same pattern: deployed for the announcement, parked after it.

Capital is behaving with caution and a healthy degree of scepticism. The market is quietly sorting protocols into three groups: those that earn revenue without needing a press release, those that keep users without paying them to stay, and those that hold up when something breaks. The five points below test for all three.

What BlackRock's BUIDL Actually Tells Us About DeFi Readiness in 2026

Of the eight blockchains BUIDL is deployed on, only two show any active DeFi deployment, Ethereum ($15.6M) and Polygon ($3.2M). Aptos, BSC, Solana, Avalanche, OP Mainnet, and Arbitrum sit at exactly zero.

Six chains have been given a blockchain address. None of them have been given a reason to use it yet. This is not a criticism of BlackRock. A $2.5 billion fund manager moving slowly into unproven rails is rational capital allocation. But it is the most honest data point available on where institutional confidence in DeFi infrastructure actually sits in April 2026 — and it is 0.75%.

Why Most Crypto Audit Frameworks Miss the Point

A traditional audit checks if the code is safe. That is a good start, but it is not enough.

A real infrastructure audit asks a different question: does anyone actually use the thing?

BUIDL is not an outlier. It is a microcosm of the entire Real World Asset (RWA) category. Analysts are forecasting anywhere from $100 billion by year-end to $2 trillion by 2030. According to DefiLlama, RWA market cap was $28.4B a year ago and sits at $28.2B today. Six months ago it peaked at $48.5B and has dropped sharply since.

The token exists. The infrastructure to use it does not.

That is the gap a five-point audit closes.

The Difference Between Crypto Fees and Revenue (And Why It Matters)

Point 1: How Protocol Revenue Determines Token Value

The first mistake most people make is confusing fees and revenue. They are not the same thing.

Fees: Every time someone borrows, trades, or moves assets through a protocol, the protocol charges a small percentage. That total — across all transactions — is the fee number

Revenue: What the protocol actually keeps after paying liquidity providers, stakers, and depositors

Aave V3 generates about $61M in fees over 30 days but keeps only $7.9M as revenue. That is a 13% margin. Aerodrome generates $6.1M in fees and keeps all $6.1M. That is a 100% margin. Same word, very different businesses. As covered in The Top 3 DeFi Protocols,

Aave passes most fees back to depositors while Hyperliquid keeps nearly 90% for its token holders. Both are working. They just work differently. If a project shows you fees but hides revenue, ask why.

Point 2: Price-to-Sales Ratio in Crypto: What It Reveals About DeFi Valuations

Stock analysts use a number called Price-to-Sales (P/S) to measure whether a token is cheap or expensive relative to what the protocol actually earns.

Low P/S: The token is priced cheaply relative to what the protocol earns — potential value

High P/S: Buyers are paying for brand or hype, not current earnings — the math has left the building

Infinite P/S: The protocol has no revenue at all. There is no math to back it up

Here are five protocols, ranked by P/S as at April 27, 2026 (point-in-time snapshot, figures move daily):

Protocol | 30-day Revenue | Market Cap | P/S Ratio |

Aerodrome | $6.1M | $437M | 5.9x |

Sky (MakerDAO) | $14.6M | $2.0B | 11.7x |

Aave V3 | $7.9M | $1.5B | 15.3x |

Maple Finance | $1.3M | $297M | 19.2x |

Uniswap V3 | $3.2M | $2.1B | 54.2x |

Uniswap at 54x is not necessarily wrong — but it means buyers are paying for the brand, not the earnings. A project with no revenue at all has an infinite P/S. There is no math to back it up.

The P/S ratio is imperfect in crypto.

One important caveat. In traditional markets, owning a share means owning a claim on earnings. In DeFi, owning a token does not always mean the protocol's revenue flows to you — some protocols pay depositors, some fund treasuries, some burn tokens. The relationship between revenue and token value is not always direct.

As a result, P/S is not a precision instrument but a smoke detector. A protocol trading at 54x P/S with growing revenue is a conversation worth having. A protocol trading at 500x P/S with no revenue at all is a warning the market has stopped asking questions. The ratio does not tell everything. It signals when something is worth a closer look and when something should stop the analysis cold.

Point 3: When Crisis Hits, Infrastructure Either Holds or It Does Not

Marketing will often disappear in a crisis. Infrastructure either holds or it does not.

The clearest live example happened eight days ago. The Kelp DAO hack on April 18, 2026 minted $292M in unbacked rsETH tokens, creating up to $200M in bad debt concentrated on Aave's lending markets. A forged bridge message minted unbacked collateral, drained Aave’s lending markets, and triggered a cascade across multiple protocols, including Aave markets and Lido-linked collateral.

Several protocols were affected in the blast radius. Most went quiet. Aave did not.

Here is what happened next:

TVL collapse: Aave's TVL fell 37% in three days, dropping from $26.4B to $16.6B

Governance response: Aave's Guardian froze rsETH markets within 77 minutes, with full remediation planning published inside 48 hours

Treasury depth: With $181M in reserves, Aave held significant internal capital, though external backstops were still required to fully absorb the bad debt

Revenue continuity: $61M in monthly fees kept generating throughout the crisis

Aave held because the response was built before the exploit happened. None of this was improvised — it was governance infrastructure stress-tested before it was needed.

Most protocols do not fail loudly. They disappear quietly. The audit is not whether something bad happens. It is what happens after.

Point 4: Test What Happens When the Incentives End

Most protocols pay users to deposit money. They give out tokens as rewards. This is called incentivised TVL.

The test is simple: what happens when the rewards stop?

This is the difference between rented liquidity and earned liquidity. Rented liquidity leaves the moment the rewards slow. Earned liquidity stays because the product works.

Lido is a liquid staking protocol. Users deposit ETH, receive stETH in return, and keep earning staking rewards without locking capital. No token incentives. Lido holds nearly $22B in deposits because the product works. That is earned liquidity.

The same test applies at the chain level. When incentives dry up across an entire ecosystem, capital leaves. Here is what that looks like in practice — TVL change across major chains over the last 90 days, according to DefiLlama:

Ethereum: TVL down 34.5% in 90 days to $45.3B — the largest absolute capital exit of any chain in the dataset

Arbitrum: TVL down 39.9% in 90 days to $1.7B — steeper than Solana, with no comparable narrative headwind to explain it. ARB token emissions have been winding down and deposits followed directly

Solana: TVL down 31.3% in 90 days to $5.6B — the meme coin cycle unwound and the capital that came with it left the same way

To put the TVL drop in context, Ethereum's market cap sits at roughly $280B on April 27, 2026, while its DeFi TVL is $45B. Only 16 cents of every dollar of ETH value is actively deployed in DeFi protocols. The rest sits in wallets. A 34.5% drop in TVL means the portion that was working got smaller.

The chains growing over the same period tell a different story:

Tron: Up 26% in 30 days — not a DeFi story but a payments story. $85.5B in USDT is held on Tron, making it the largest single-chain stablecoin balance in the world, serving cross-border settlements, remittances, and OTC trades. Most Western analysts do not track it.

Base: Up over 80% in the past year — Coinbase built the distribution first, then built the chain around it. Users followed the product they already trusted.

Hyperliquid: Up over 100% in the past year — Hyperliquid built its own L1 from scratch, charges zero gas fees, and processes perpetual trades faster than any centralised exchange competitor. In Q1 2026 alone it returned $192M to token holders through buybacks, the highest distribution rate of any protocol in the top ten. No liquidity mining. No token incentives. A trading product that retained users because it was faster and cheaper than the alternative.

This is not a ranking of best chains. It is a snapshot of where usage held when the rewards stopped and where it did not.

Point 5: Verify the Audits Are Still Valid

An audit stamp is only as good as the date on it. Most users never check the date.

A 2021 audit means nothing if the code has been upgraded twelve times since 2021. A trusted auditor on an old version of a protocol does not protect users from new bugs.

Three things to check:

Audit recency: When was the last audit relative to the last major code change? A 2021 stamp on a protocol that has shipped twelve upgrades since means nothing

Open source: Is the code public and verifiable by anyone? Closed source code cannot be independently checked, only trusted

Battle tested: Has the protocol survived a real exploit, market crash, or liquidation cascade? Protocols that have only ever run in good conditions, or have not completed a full four-year cycle, have never been audited by reality.

Tether spent years under a cloud because no major auditor would touch it, and the market priced that uncertainty into every institution that held it. Tether's KPMG audit engagement, announced in March 2026, changed that calculus. Not because the results are in — they are not — but because a Big Four firm putting its name to the process signals that Tether believes its reserves will withstand scrutiny. That is the floor. Anything below it is trust without evidence.

How to Audit a DeFi Protocol: A Practical Checklist for 2026

Investors can run the following checks before deploying capital into any protocol:

Check | Green Flag | Red Flag |

Revenue disclosed? | Yes, on-chain verifiable | Only TVL or fees cited |

P/S ratio | Under 20x with growing revenue | No revenue or infinite multiple |

Crisis history | Survived at least one stress event | Only ever ran in good markets |

TVL without incentives | Holds or grows | Collapses when rewards stop |

Audit recency | Recent audit + open source | Old audit, closed code |

Crisis response | Public, fast, on-chain | Silent, vague, off-chain only |

Why Running a DeFi Audit Matters

Running the five-point audit takes about thirty minutes per protocol. The benefit is direct: capital protection.

Benefits of Running the Five-Point Framework Before Investing

The allocators who came out of the Kelp hack event in the best position were not the ones who predicted it. They were the ones who had already done the work. Benefits include:

Fewer negative surprises: Allocators who ran a stress-history check before April 18 knew Aave had the treasury depth, governance infrastructure, and revenue continuity to absorb the Kelp damage. They sized accordingly

Fairer entry price: Identifying P/S ratios before allocating means paying closer to fair value. Audit-led allocators rarely pay 54x for what a comparable protocol delivers at 6x

Early exit signals: Tracking incentivised vs organic TVL flags rented liquidity before the headline does. The Solana and Arbitrum contractions were visible in the data weeks before they became market news.

Risks of Skipping the Framework

Skipping the framework does not eliminate the risks. It just moves the discovery date to the worst possible moment. Risks involved:

Stress-event exposure: Allocating a protocol that has never been tested in a crisis means finding out the hard way, usually at 3am reading headlines wondering whether to exit.

Inflated multiples: Buying a token at 54x P/S when comparable protocols trade at 6x means paying a premium for the brand. The market corrects these gaps. The investor absorbs the correction.

Rented-liquidity collapse: When incentives end, capital flees. Solana lost 31% and Arbitrum nearly 40% of TVL in 90 days for exactly this reason. The audit catches it before the position does.

Where Crypto Infrastructure Is Quietly Winning in 2026

The most interesting story in DefiLlama's April 2026 data is where the marketing is not.

Tron: $85.5B in USDT held on-chain with almost zero USDC. This is not a DeFi story but a remittance story. Workers send money home. Businesses settle invoices. Most Western analysts do not track it.

Provenance: A blockchain built for institutional finance, up 72% in the last 90 days. Its native token HASH trades at a $608M market cap, small relative to $1.6B in chain TVL, and largely ignored by the market narratives driving token price action elsewhere. Almost nobody on crypto Twitter talks about it

Hyperliquid: Built its own L1 from scratch, runs the most capital-efficient trading platform in the top ten, and returned $192M to token holders in Q1 alone — as covered in the Top 3 Protocols breakdown.

The infrastructure winning right now is not the infrastructure being marketed. It is the infrastructure being used.

Running the audit does not make the next crisis predictable. It makes the position survivable.

Knowing which protocol passes the five-point check is half the work. The other half is knowing when to enter. Aping into a sound protocol at the wrong price is still a loss. The Coinjuice trading framework covers exactly that: how to identify entry points without leverage, without liquidation risk, and without guessing.

Conclusion

Most crypto reporting still measures things by what happened on Twitter. The five-point framework measures things by what happened on-chain.

Real protocols generate real revenue. Real infrastructure holds during a real crisis. Real adoption survives the day the incentives stop. Real audits are recent and verifiable.

Run the five points before allocating capital. If a project passes all five, it is doing the work. If it fails three or more, the marketing is doing the work.

Auditing crypto infrastructure in 2026 does not require an expensive terminal or a legal team. It requires five checks, thirty minutes, and the willingness to look at what the chain actually shows rather than what the marketing says. The framework is free. The data is public. The only thing most people skip is the audit itself.

FAQ

What is the main goal of the five-point framework for auditing crypto infrastructure in 2026?

The framework aims to close the gap between tokens that exist and infrastructure that is actually used, by testing whether protocols generate real revenue, retain users without incentives, and hold up during crises, based on on-chain data rather than marketing.

How does the framework distinguish between fees and revenue, and why is that important?

Fees are the total charges collected on protocol activity, while revenue is what the protocol keeps after paying liquidity providers, stakers, and depositors. This matters because two protocols with similar fees can have very different business models and token value, depending on how much of those fees they retain.

What is the difference between rented liquidity and earned liquidity in DeFi?

Rented liquidity comes from users who deposit funds mainly to earn token incentives and leave when rewards slow, while earned liquidity stays because the product works without incentives, as shown by Lido holding nearly $22B in deposits with no token rewards.

Which checks does the practical DeFi audit checklist recommend before allocating capital to a protocol?

The checklist recommends verifying that revenue is disclosed and on-chain verifiable, that the P/S ratio is under 20x with growing revenue, that the protocol has survived at least one stress event, that TVL without incentives holds or grows, that audits are recent and code is open source, and that crisis responses are public, fast, and on-chain.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

More like this

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.