Quick summary

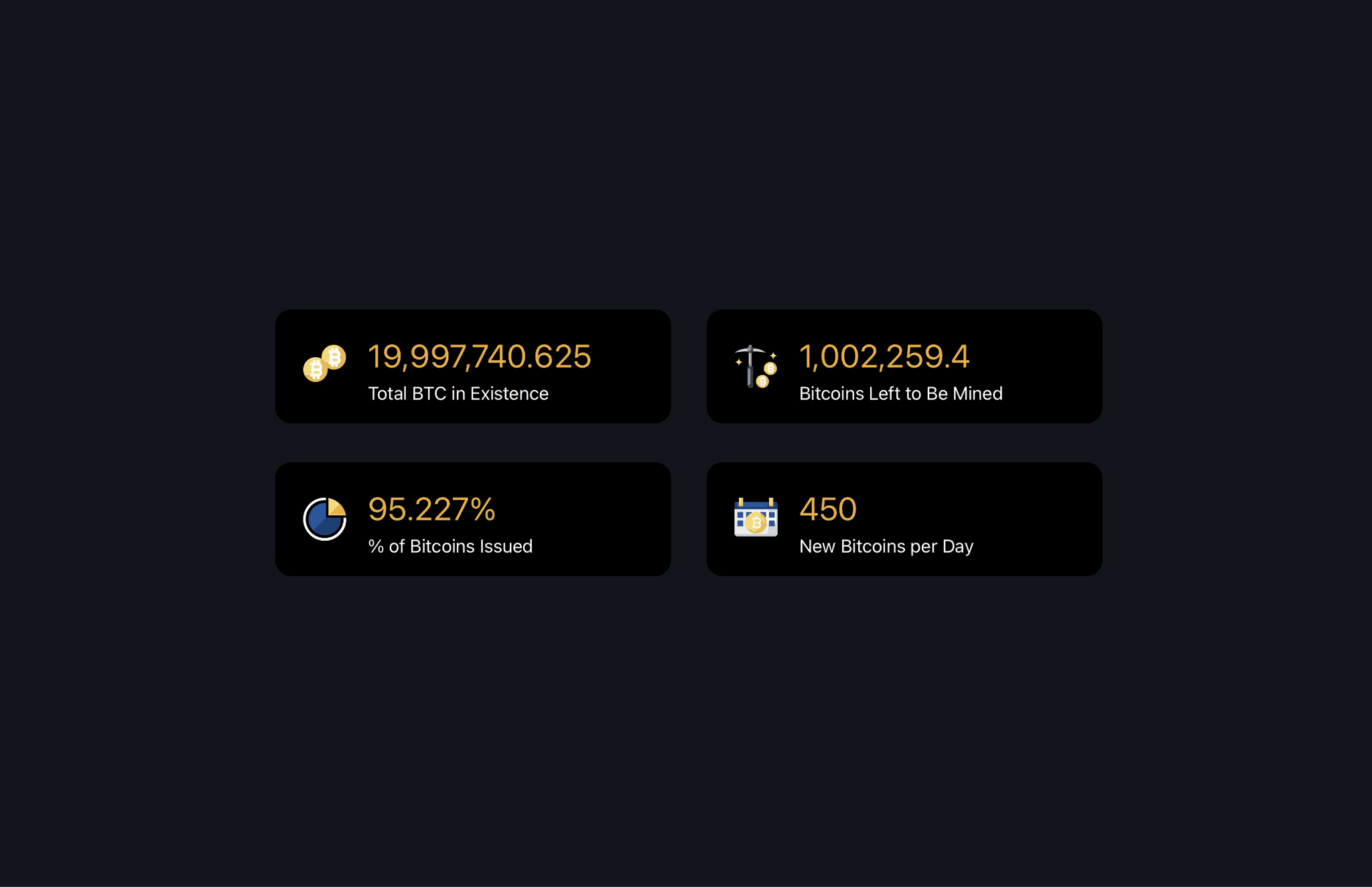

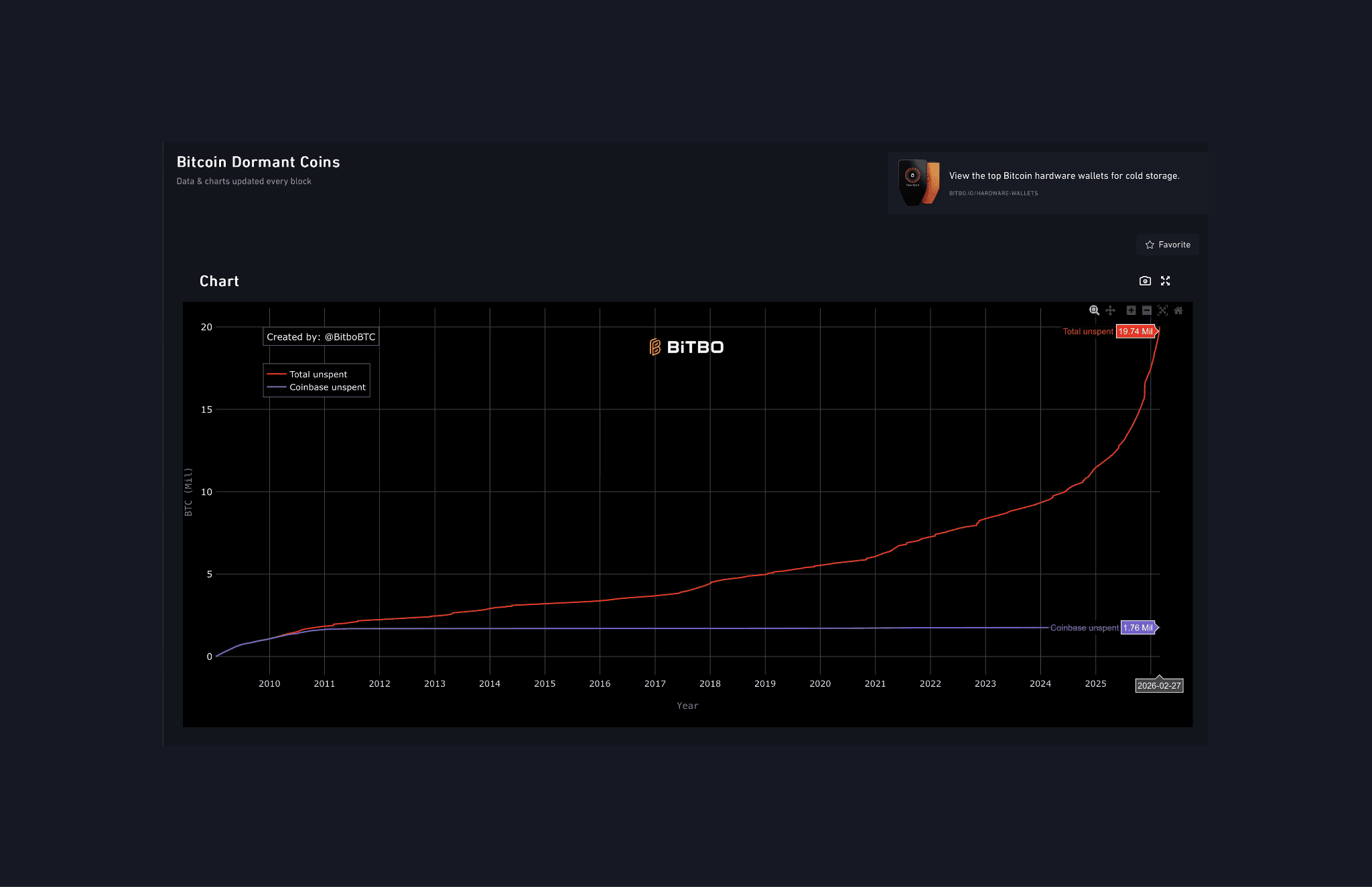

Approximately 19.9 million Bitcoin had been mined by 2026, leaving roughly one million coins remaining to be issued

Effective circulating supply is far smaller than headline supply due to long-term illiquid holdings and permanently lost coins

Halvings progressively reduce new issuance, with daily block rewards expected to fall to single digits around 2049

The long-term transition to a fee-only mining model raises questions about network security and the durability of Bitcoin’s fixed supply

Of the 21 million Bitcoin that will ever exist, approximately 19.9 million of the 21 million has been mined by March 2026, leaving roughly 1,002,259 coins remaining. New Bitcoin is currently issued at about 450 BTC per day under a halving schedule that reduces the rate every four years until issuance ends around the year 2140. That final million is a subtle but active economic force reshaping miner incentives, compressing liquid supply, and hardening the scarcity premium already priced into a $1.43T market.

This article examines what Bitcoin’s final million supply means for price volatility, reviews research on network security in a fee-only mining environment, maps the halving roadmap through Bitcoin’s first 40 years, and considers the governance decisions that will determine whether Bitcoin’s fixed supply remains its greatest strength or becomes its most tested assumption.

Bitcoin Scarcity Is No Longer Theoretical: It's Happening Now in 2026

On March 4, 2026, 95.2% of all Bitcoin that will ever exist has already been issued.

The remaining 4.8% will take over 100 years to mine, shrinking in availability with every halving cycle. Compare that to gold, where annual mining adds roughly 1.5–2% to total supply each year indefinitely. Bitcoin has no such release valve with characteristics including a:

Hard cap: 21,000,000 BTC, protocol-enforced, requiring global consensus to alter

Coins remaining: ~1,002,259 BTC as of early March 2026

Daily issuance: 450 BTC per day (3.125 BTC per block × ~144 blocks) a rate that halves again in 2028

Illiquid supply: A 2025 peer-reviewed supply-demand model found that genuinely liquid Bitcoin coins actually available to trade may already sit closer to 3 million, not the full 19.9 million in circulation being available, with the critical scarcity threshold placed at approximately 2 million liquid coins (Rudd & Porter, 2025). The study describes the 2M threshold as the point where "marginal purchases move price disproportionately" and refer to it throughout as the Bitcoin "scarcity corridor."

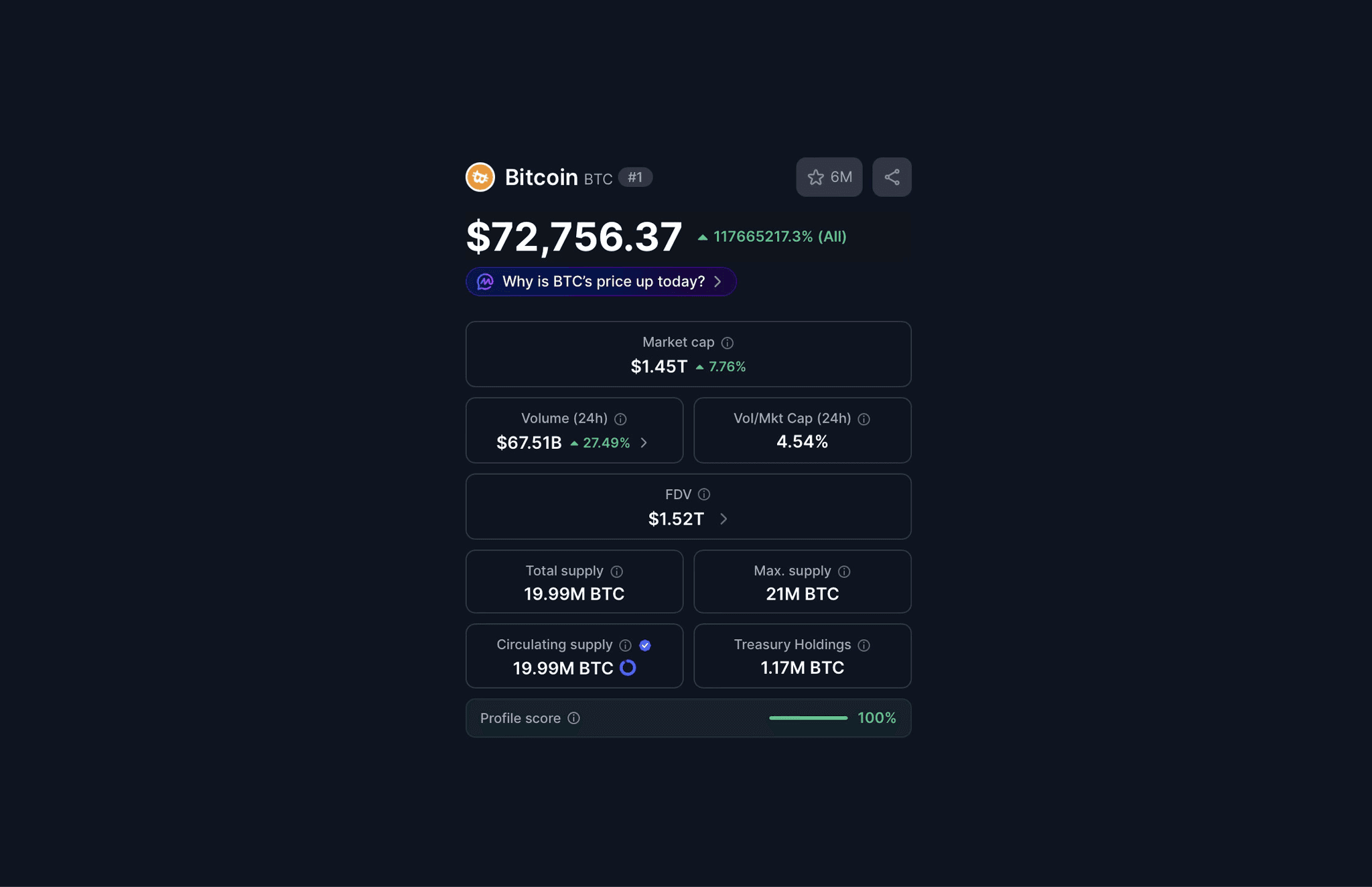

The current price of $71,786 per BTC with a $1.43T market cap reflects a market that already prices in scarcity. What the final million introduces is an acceleration of that dynamic.

What Bitcoin's Market Cap Tells Us About Where Bitcoin is in 2026

Bitcoin's fully diluted valuation (FDV) sits at $1.5T the value the market assigns if all 21 million coins were already in circulation.

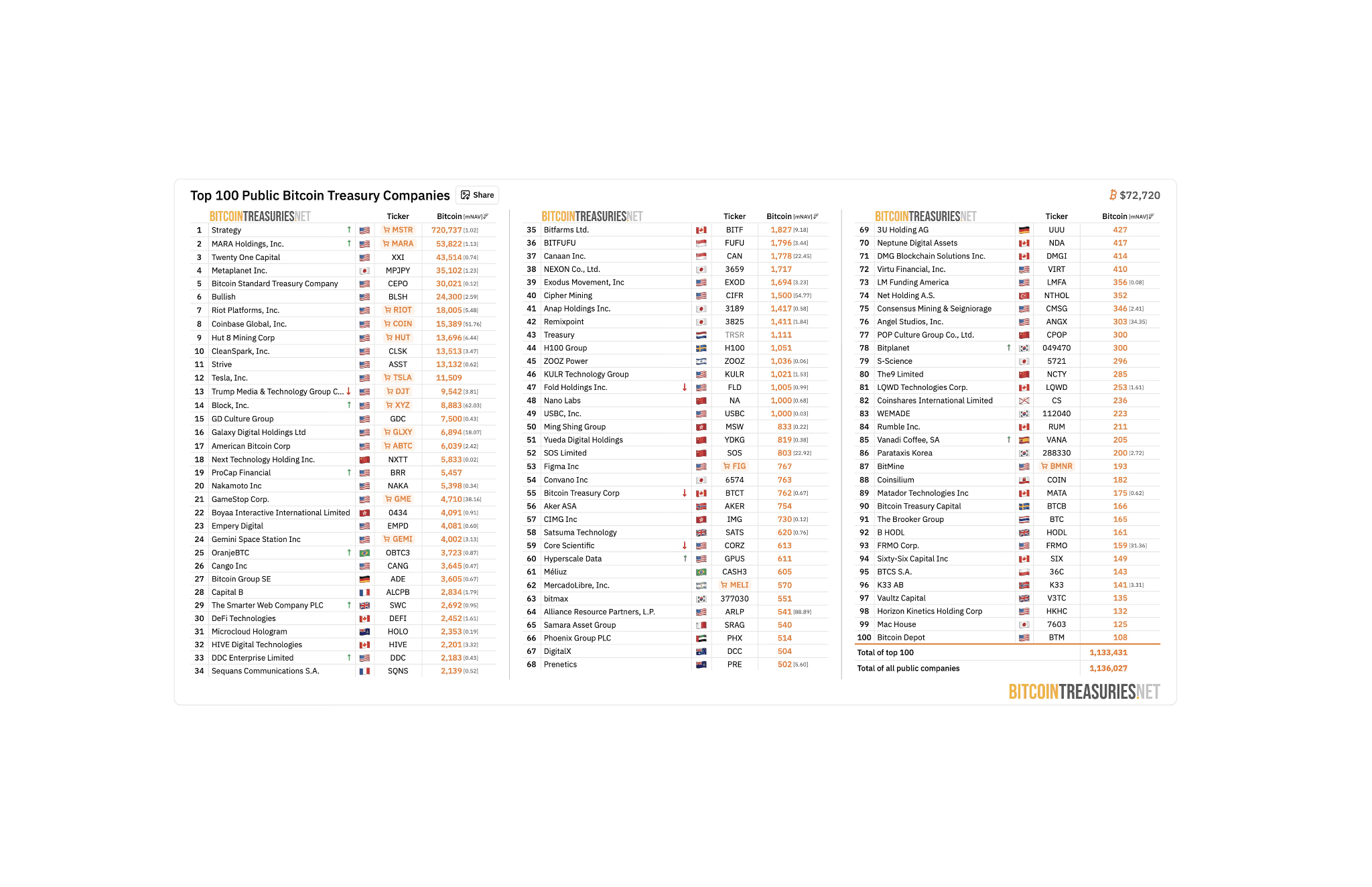

Bitcoin’s current $1.43T market cap sits less than $70B below its $1.5T fully diluted valuation. Meanwhile, public companies alone hold more than 1.13 million BTC, led by Strategy’s 720,737 BTC and nearly 100 listed firms steadily absorbing supply faster than miners can produce it. Current market demand can be seen in the following metrics:

Market cap: $1.43T (up 7.82% in the most recent recorded period)

24h trading volume: $65.16B with roughly 4.54% of total market cap turns over daily

Treasury holdings: 1,136,027 BTC held across public company balance sheets alone, with Strategy accounting for 720,737 BTC (figures sourced from BitcoinTreasuries.net)

All-time return: 116,096,554% one of the highest asset returns recorded in modern financial history as recorded by CoinMarketCap from Bitcoin's earliest tracked price to March 2026.

The Lost Coins Problem: Why the Final Million May Already Be Gone

On-chain supply figures show approximately 19.9 million Bitcoin in existence.

What those figures cannot show is how many of those coins are permanently inaccessible, lost to forgotten wallet keys, early miner inactivity, and hardware failures from Bitcoin's first decade.

Estimates from multiple on-chain analytics firms place lost or permanently dormant Bitcoin between 3 and 4 million coins. If accurate, the effective circulating supply is closer to 16–17 million and not 19.9 million. This single fact reframes Bitcoin’s entire scarcity thesis in the following:

Estimated lost BTC: 3–4 million coins, based on long-term dormancy and wallet analysis

Effective circulating supply: Approximately 16–17M BTC by conservative estimates

Satoshi's coins alone: Roughly 1.1M BTC mined in Bitcoin's earliest blocks have never moved with their status as lost, held, or deliberately dormant remains unknown

Practical implication: The "final million" being mined may represent a far larger share of genuinely active supply than the 4.8% remaining figure suggests

Scarcity multiplier: If 3–4M coins are permanently removed from circulation, every remaining accessible Bitcoin becomes proportionally scarcer a factor not reflected in standard supply metrics

The lost coin estimate is inherently imprecise.

Coins that appear dormant can move. Yet the directional argument holds: accessible Bitcoin supply is meaningfully smaller than total issued supply, and that gap widens the scarcity case for the coins that remain.

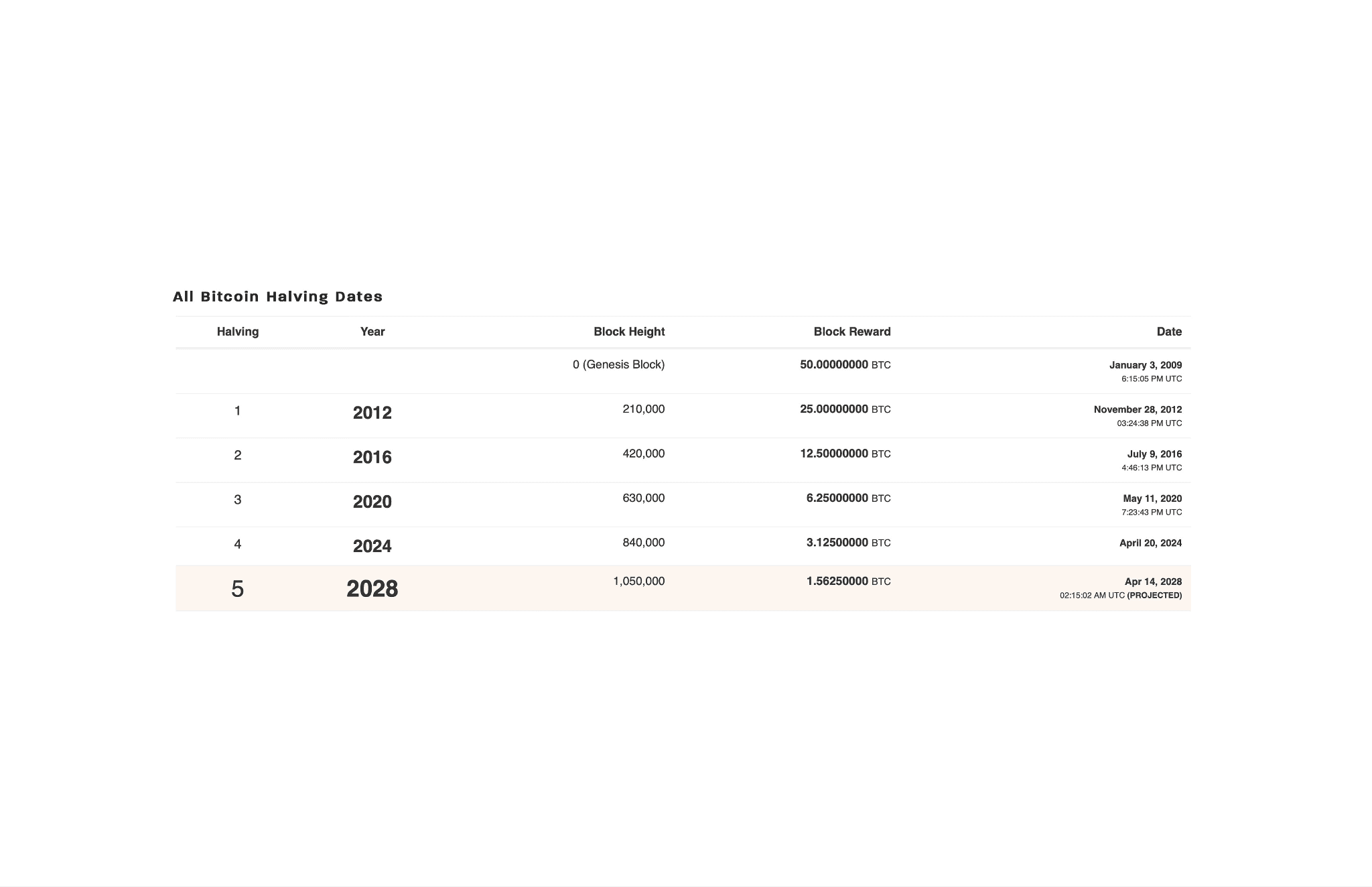

Bitcoin Halving Roadmap: How Much Supply Is Left at Every Stage

Every four years, Bitcoin's block reward halves.

Each halving cuts daily issuance in half and extends the timeline to full supply. The table below maps remaining supply, daily issuance, and cumulative percentage issued at each halving from now through Bitcoin's first 40 years.

Halving | Approx. Year | Block Reward | Daily Issuance | Est. BTC Remaining | % of 21M Issued |

Current (post-4th) | 2024–2028 | 3.125 BTC | ~450 BTC | ~1,002,259 | ~95.2% |

5th Halving | 2028 | 1.5625 BTC | ~225 BTC | ~673,000 | ~96.8% |

6th Halving | 2032 | 0.78125 BTC | ~112 BTC | ~509,000 | ~97.6% |

7th Halving | 2036 | 0.390625 BTC | ~56 BTC | ~427,000 | ~98.0% |

8th Halving | 2040 | 0.1953125 BTC | ~28 BTC | ~386,000 | ~98.2% |

Bitcoin Age: 40 Years | ~2049 | ~0.049 BTC | ~7 BTC | ~357,000 | ~98.3% |

Note: Estimates based on ~144 blocks per day and current mining pace. Actual figures vary with block time variance with remaining supply figures being approximate and compound across halvings.

What the table above shows: the compression is asymptotic. Which means a straight line that continually approaches a given curve but does not meet it at any finite distance. Each halving cuts issuance by half, but the remaining supply shrinks slowly, meaning the final coins take decades to issue.

By Bitcoin's 40th birthday year (approximately 2049), over 98% of all supply will be in circulation, with daily issuance reduced to single digits. Cross-reference that with 3–4M estimated lost coins and the picture of accessible scarcity becomes sharper still. By the year 2049 only 357,000 BTC will be left to be mined.

Mining Security in a Fee-Only World

Bitcoin miners currently earn a block subsidy, newly created coins, plus transaction fees. The subsidy halves roughly every four years. After the final million coins are mined, the miner subsidy reaches zero, and miner revenue will depend entirely on what users pay to transact.

Research by Budish (2025, Oxford Academic) and Carlsten et al. (Princeton) identifies a structural risk in this transition:

Fee-only regime: Once block subsidies disappear, miner revenue depends entirely on transaction fees, which fluctuate with network demand, creating revenue uncertainty that affects hash power investment decisions

Undercutting attacks: Carlsten et al. (2016) proved through game-theoretic analysis and a purpose-built Bitcoin mining simulator that in a fee-only regime, miners have a rational incentive to deliberately fork the chain, withholding transactions and undercutting the previous block's fees to attract other miners to build on their version instead. Critically, the paper found this strategy becomes profitable even when two thirds of miners remain honest, meaning a minority of strategic miners is sufficient to destabilise consensus and create a growing backlog of unconfirmed transactions

Hash power erosion: As long-term mining rewards decline, marginal miners exit the market, reducing the total computing power securing the network against attack

Confirmation finality: Hasu, Prestwich & Curtis (2019) argue that once subsidies wane, overall hash power and fee-per-hash dynamics become the primary determinants of transaction finality not block confirmation count alone

Proposed solutions: Tail subsidies (small permanent inflation), dynamic block sizes, fee-burning mechanisms, and user-sponsored transaction crowdfunding are all under academic discussion; none are currently adopted in Bitcoin's protocol.

Bitcoin Governance Will Face Its Hardest Test

Bitcoin's fixed supply is its most politically charged feature. Any proposal to alter it, even a small perpetual issuance designed to fund miner security, requires consensus across a deeply decentralised global community. That conversation is already beginning in academic and developer circles:

On-chain governance proposals: Academic literature is beginning to explore decentralised mechanisms, including algorithmic fee-market adjustments, to stabilise miner incentives as subsidies decline, though no formal governance framework has yet been adopted by the Bitcoin protocol

Regulatory attention: Policymakers are beginning to examine what declining miner economics mean for financial stability and AML enforcement, an area with almost no formal academic treatment yet, representing a genuine research gap

Protocol conservatism: Bitcoin's development culture favours minimal changes; any security-motivated protocol amendment faces an exceptionally high bar for community adoption

The core tension: A fixed supply is Bitcoin's most valued property and the halving roadmap above shows how slowly that supply releases, making the fee-transition timeline longer than most assume

Conclusion

The final million Bitcoin is an active economic variable already reshaping how the network functions. Liquid supply is tighter than headline figures suggest, institutional absorption is outpacing daily issuance, and the halving schedule will keep compressing both until issuance reaches single digits or 7 BTC per day around 2049.

This article has mapped the structural conditions behind Bitcoin's final million supply:

Hard cap: 21 million coins with no release valve, protocol-enforced and requiring global consensus to alter

Liquid float: Peer-reviewed modelling places genuinely tradeable supply closer to 3 million coins than the 19.9 million headline figure implies, with a critical scarcity threshold at approximately 2 million

Fee-only security: Research from both economics and computer science identifies the transition away from block subsidies as Bitcoin's most consequential unsolved problem, one that no protocol change has yet addressed

The scarcity thesis requires only that the numbers stay what they are and on the supply side, they are locked in code. The open question is whether the governance, security infrastructure, and fee markets mature fast enough to meet the economic endgame the halving schedule is quietly, mechanically, building toward.

FAQ

How many Bitcoin remain to be mined in 2026, and how fast are new coins being issued?

As of early March 2026, about 19.9 million Bitcoin have been mined, leaving roughly 1,002,259 BTC remaining. New Bitcoin are issued at about 450 BTC per day (3.125 BTC per block across ~144 blocks per day) under a halving schedule that reduces issuance roughly every four years until around 2140.

What is Bitcoin’s ‘liquid supply’ and the ‘scarcity corridor’?

A 2025 peer-reviewed model estimates that genuinely liquid Bitcoin actually available to trade may be closer to 3 million coins, rather than the full 19.9 million in circulation. It identifies a critical scarcity threshold at approximately 2 million liquid coins, described as the “scarcity corridor,” where marginal purchases move price disproportionately.

What is the lost coins problem and how does it affect effective Bitcoin supply?

On-chain data show about 19.9 million BTC exist, but multiple analytics firms estimate 3–4 million may be lost or permanently dormant. This implies an effective circulating supply of roughly 16–17 million BTC. If those coins are permanently removed, every remaining accessible Bitcoin becomes proportionally scarcer, and the newly mined “final million” may represent a larger share of genuinely active supply than the 4.8% headline figure suggests.

What security and governance challenges arise as Bitcoin moves toward a fee-only mining regime?

As block subsidies halve and eventually reach zero, miner revenue depends entirely on transaction fees, which fluctuate with demand and create revenue uncertainty, hash power erosion, and new attack incentives such as undercutting attacks that can be profitable even if two thirds of miners remain honest. Research suggests transaction finality will hinge on overall hash power and fee-per-hash. Proposed mitigations—like tail subsidies, dynamic block sizes, fee-burning, and user-sponsored crowdfunding—are under academic discussion but not adopted. Because Bitcoin’s fixed 21 million cap is politically charged and protocol changes face high resistance, any security-motivated modification would require broad consensus across a decentralised global community.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

More like this

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.