Quick summary

Derive is a DeFi derivatives exchange, DRV governs, earns fee share, and discounts trading

DRV has 1.5B max supply, 737.52M circulating, with emissions and significant future unlock overhang

35% of protocol fees fund weekly DRV buybacks, partially offset by ongoing staking emissions

Top 10 wallets hold 82.55% on-chain DRV, creating notable holder concentration and liquidity risk

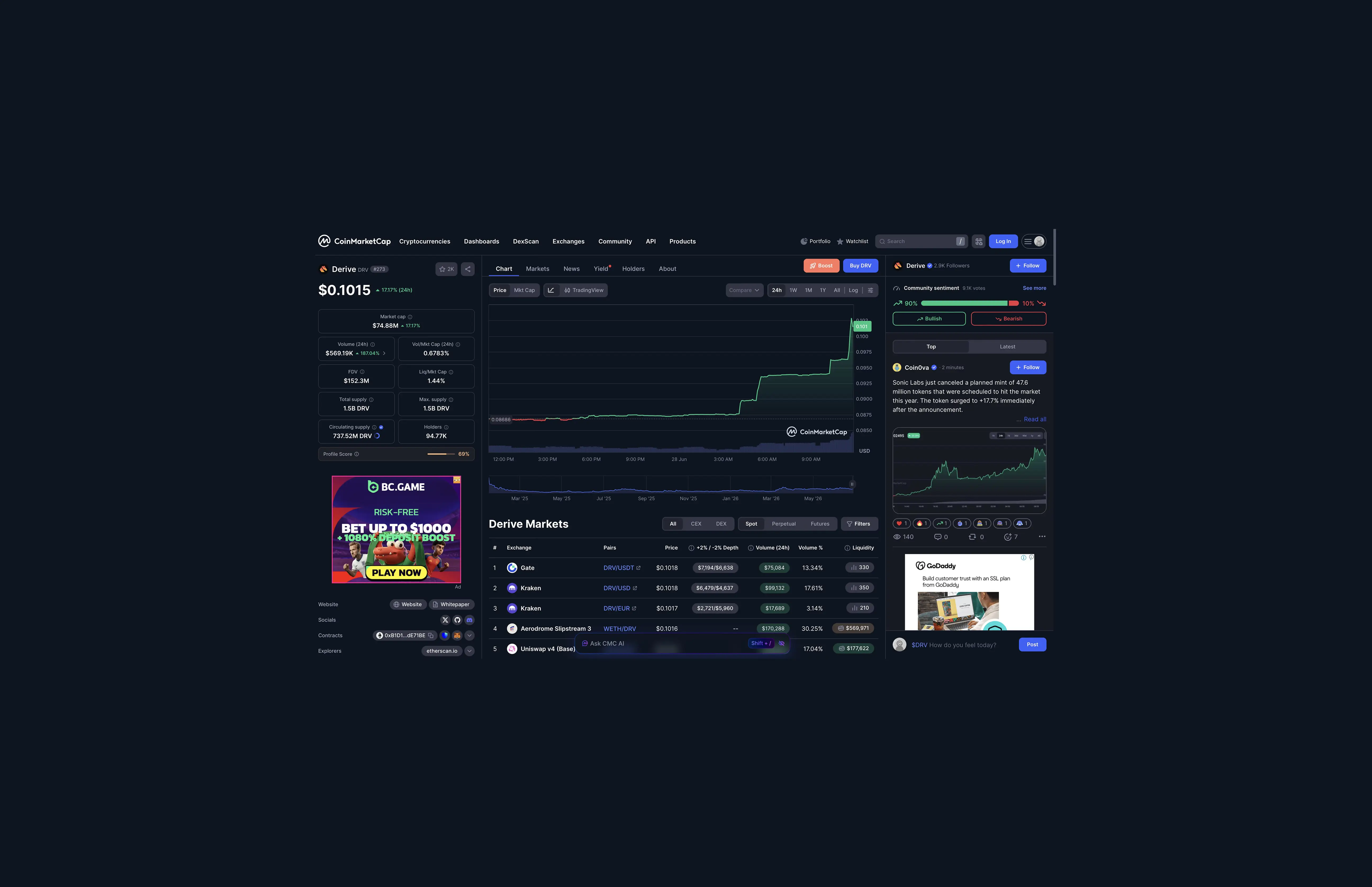

Price: $0.1015 | Market Cap: $74.88M | Circulating Supply: 737.52M DRV | Max Supply: 1.5B DRV | FDV:$152.3M (Source: CoinMarketCap, 28 June 2026)

Derive launched its DRV token on January 15, 2025 built on infrastructure the team had been developing since 2021 under the name Lyra Finance and is a crypto trading platform where you can trade options, perpetuals, and spot, all from a wallet the individual owns. The platform has a token called DRV, which earns a share of trading fees, gives holders a vote on how the protocol runs, and gets bought back and removed from circulation using the revenue the platform generates.

This article covers what DRV is, how its tokenomics are structured, whether the buyback mechanism creates scarcity, and what the holder distribution reveals about concentration risk. Like any crypto analysis, this is one coin among thousands picked because the chart structure looks interesting and the fundamentals clear a basic bar. That does not make it a recommendation.

Crypto is speculative by nature, most tokens do not survive long term, and this one is no exception to that risk. Read it with that in mind.

What DRV Actually Is and What This Article Does

Worth knowing upfront: the current market cap is $74.88M based on tokens in circulation today, but the fully diluted valuation, what the market cap would be if every token that will ever exist was already live, sits at $152.3M.

That gap exists because only half the total supply is currently in circulation. The rest enters the market over time through staking emissions and unlocks. if demand does not keep pace, price takes the hit.

Small-cap equals high risk. Do your own research before making any decisions.

Do your own research before making any decisions.

The purpose of this article is straightforward: to assess whether DRV is a protocol trending toward zero or one worth tracking for volatility plays. The fundamentals here, active buybacks, growing trading volume, and a real fee-generating product, suggest it clears that bar for a year or so. Whether it fits your risk profile is a separate question entirely.

Reading a chart like this without a framework is guesswork. The Coinjuice trading ebook gives you the exact method used in the PRO analysis, so you can start identifying advantageous entries and exits yourself.

What Is Derive?

Here is what the protocol actually is and how it works.

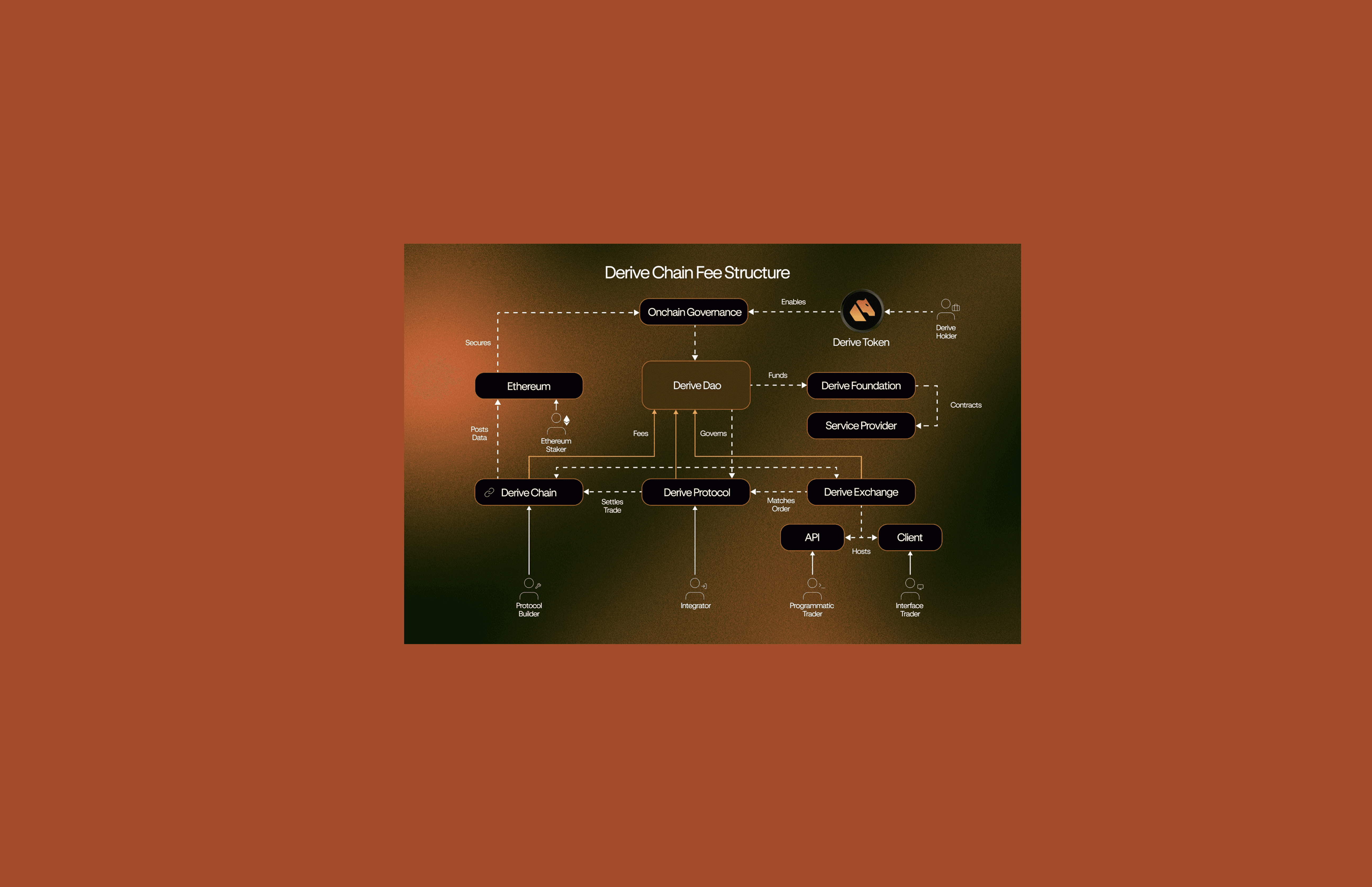

Platform type: Decentralised derivatives exchange (options, perpetuals, spot)

Infrastructure: Optimistic rollup on the OP Stack, settling to Ethereum

Orderbook: Rust-powered, off-chain matching with on-chain settlement, capable of up to 20M TPS per Derive's published specifications

Custody model: Self-custodial, users retain control of private keys throughout

Audience: Derive describes itself as built for professional traders, institutions, and market makers, offering TradFi-level execution speed on-chain

Background: Derive was previously known as Lyra Finance, a DeFi options protocol. The platform was rebuilt from an AMM model into a central limit order book and rebranded, with the DRV token replacing LYRA at a 1:1 migration ratio. DRV went live on 15 January 2025, per Derive's help centre

Derive's disclosed partners include Ethena, EtherFi, Swell, Kraken, OKX, Optimism, and LayerZero, among others listed on derive.xyz.

DRV Token: The Basics

Token standard: ERC-20 on Ethereum

Maximum supply: 1,500,000,000 DRV (1.5 billion)

Circulating supply: 737.52M DRV as of 28 June 2026

Current price: $0.1015

Market cap: $74.88M

Fully diluted valuation (FDV): $152.3M

The gap between market cap and FDV, roughly 2x, reflects the portion of supply not yet in circulation.

That remaining supply will enter the market through staking emissions and ecosystem allocations over time, which is a relevant context for anyone assessing the scarcity argument.

Token Allocation

According to Derive's published whitepaper (hosted via Kraken), the initial allocation at launch was structured as follows:

40%: Community incentives

25%: Ecosystem development

20%: Foundation reserve

15%: Strategic partners and early investors

These allocations determine where new supply enters circulation as vesting periods unlock.

How DRV Is Used

DRV serves three functions within the Derive protocol, as described in Derive's own documentation:

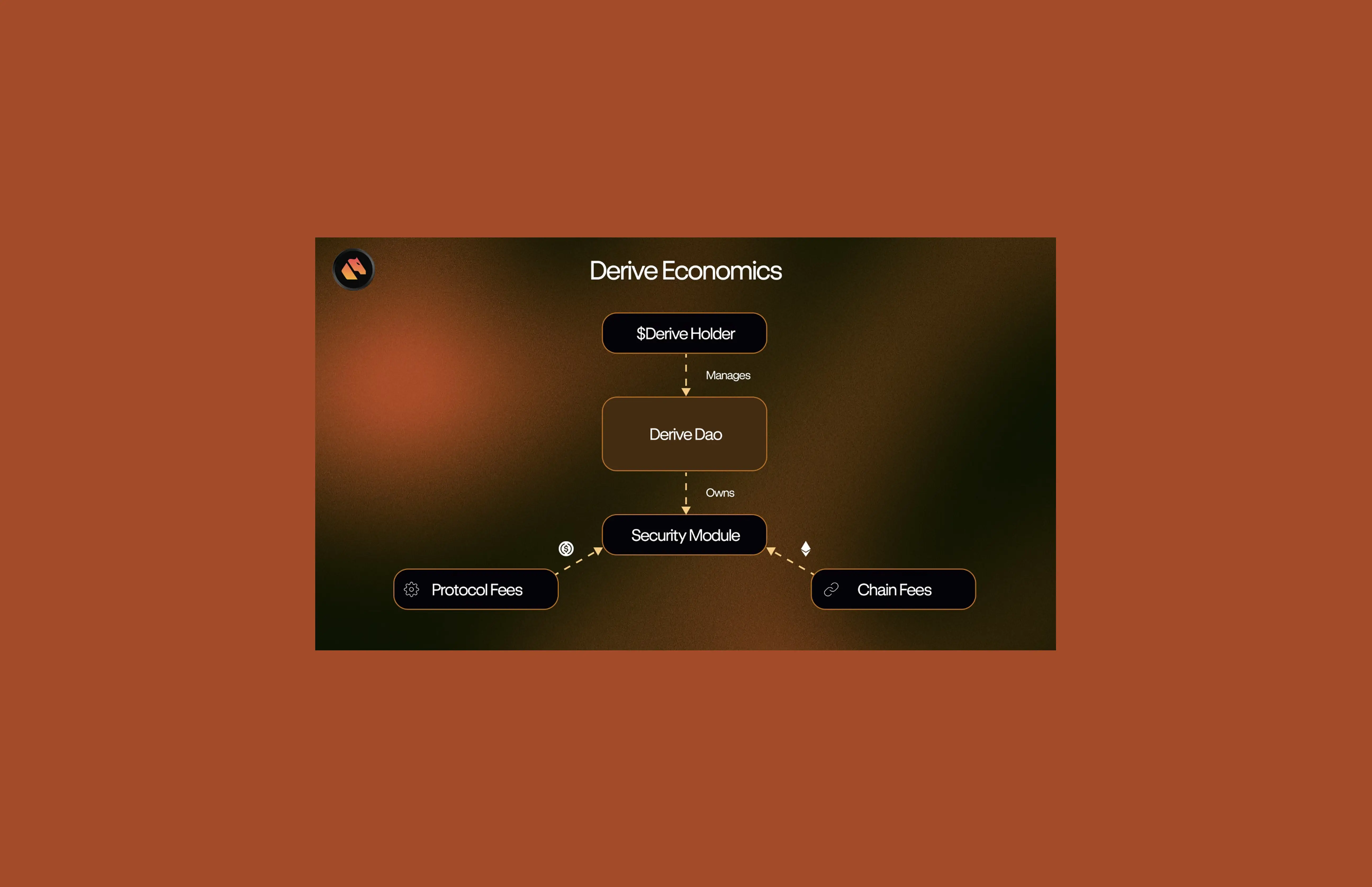

Governance: Staked DRV holders vote on protocol proposals, including fee parameters, treasury allocations, and token emission schedules. Governance operates on Derive L2. Voting power can be delegated.

Staking rewards: DRV stakers earn rewards funded by DAO emissions. Per Derive's documentation, initial weekly staking rewards were up to 1,150,000 DRV. After the first six months post-TGE, this reduces to a maximum of 600,000 DRV per week, with the rewards increasingly funded by buybacks rather than new emissions.

Fee discounts: DRV stakers receive reduced trading fees on spot, perpetuals, and options, proportional to their staked balance.

In plain terms: hold DRV, stake it, and you get a vote on how the protocol runs, a cut of the rewards it generates, and cheaper fees when you trade. For a token you are already tracking for volatility, that is a reasonable set of side benefits while you wait for a setup.

The Buyback Mechanism: How It Works

The core of the scarcity argument for DRV rests on its buyback programme. Here is what Derive has disclosed directly:

Revenue sources: The DAO earns fees from trading activity, liquidation fees, interest rate spreads, and Derive L2 rollup fees

Buyback allocation: 35% of net protocol fees are directed to DRV token buybacks (according to Derive's token documentation at docs.derive.xyz)

Execution: Buybacks are executed weekly, using protocol revenue to purchase DRV on decentralised exchanges

Repurchased to date: Over 21.3 million DRV tokens had been repurchased as of March 2026, representing approximately 2.9% of current circulating supply, with weekly buybacks continuing since

Emissions offset: At peak buyback activity in March 2026, a single week's buyback (642,831 DRV) exceeded weekly trading reward emissions (~50,000 DRV/week), meaning the protocol was buying back more than it was emitting in that period

The buyback mechanism is funded entirely by protocol revenue. If trading volume falls, fee revenue falls, and the buyback volume falls with it. The scarcity effect is contingent on sustained platform usage.

What Changed in April 2026

Derive's governance community voted to increase the buyback allocation from 25% to 35% of net fees, and simultaneously reduced weekly staking emissions from 250,000 to 100,000 DRV.

This was reported by multiple sources citing Derive's governance portal as of April 23, 2026.

The combined effect: more revenue directed toward repurchases, and less new supply entering circulation from staking.

Note: for the precise on-chain snapshot and vote breakdown, verify directly at derive.xyz/governance

Does the Buyback Create Scarcity?

This is the right question to ask, and the honest answer is: partially, in the current environment — with conditions attached.

What supports the scarcity case:

Supply cap: 1.5 billion DRV maximum though this ceiling was already raised once by a governance proposal in September 2025 to increase supply from 1B to 1.5B was submitted by co-founder Nick Forster, and the current supply cap now stands at 1.5B.

Active buybacks: Over 21.3 million DRV has been bought back and removed from circulation as of March 2026, with weekly purchases continuing since

Emissions slowing: The rate at which new DRV enters circulation is designed to decrease over time

Scales with usage: The more the platform is used, the more fees it generates, and the more DRV gets bought back

What limits the scarcity case:

FDV gap: With 737.52M DRV in circulation against a 1.5B cap, roughly 762M tokens remain to be distributed. That is a substantial unlocked supply overhang

Emission-funded staking: New DRV is still being created for staking rewards, which partially offsets buyback-driven reductions

Revenue dependency: Buybacks stop if protocol fee revenue dries up. There is no programmatic burn independent of trading activity

No autonomous burn: Unlike protocols that burn a fixed percentage of transaction fees automatically, Derive's supply reduction is entirely governance-directed. The DAO could reduce or pause buybacks through a future vote

DRV Holder Distribution: What the Data Shows

On-chain data for DRV on Ethereum as of 28 June 2026 (sourced from the CMC holders tab) shows the following:

Top 10 wallets hold 82.55%: of on-chain circulating supply

Wallet #1 alone holds 53.65%: 456.91M DRV valued at $46.44M

Wallet #2 holds 7.13%: 60.71M DRV

All other holders combined: 17.45%

This level of concentration is notable. A single wallet holding over half the on-chain supply means that a decision to sell, transfer, or redistribute from that address would have a meaningful impact on market liquidity.

One important caveat: this data reflects Ethereum mainnet holdings only. Derive operates its own L2 chain, where additional DRV may be held by active traders and stakers. The Ethereum on-chain snapshot does not capture the full distribution picture across all chains.

The concentration figure is relevant to the scarcity argument in one specific way: if the top wallet represents a foundation or treasury address that is locked or vesting, it does not represent immediately circulating supply. If it is a freely transferable address, it represents a single point of liquidity risk.

Protocol Activity: Context for the Buyback Thesis

The buyback thesis depends on fee revenue. Here is what is publicly known about Derive's activity as of mid-2026:

TVL: $109.3M (DefiLlama, Derive V2, 28 June 2026)

Weekly options volume peak (March 2026): Approximately $294M notional in a single week during elevated market volatility

Weekly volume by early June 2026: $707M per week, per Derive's published figures

Largest single trade: A $130M+ notional BTC options structure, described at the time as the largest on-chain options trade on record

Coinbase listing: DRV began trading on Coinbase on 27 May 2026, its largest centralised exchange listing to date

Who Is Derive Actually Competing Against?

Derive operates in the crypto derivatives market, a space dominated by centralised exchanges and largely untouched by decentralised alternatives until now. Here is who holds the ground it is trying to take.

Deribit: The incumbent. Controls approximately 80% of all global crypto options volume and was acquired by Coinbase for $2.9 billion in 2025 the benchmark Derive's entire institutional thesis is measured against.

Aevo: The closest structural peer on-chain. Also built on an OP Stack L2, also offers options and perpetuals, also no KYC. TVL has fallen to approximately $15M and fee revenue is no longer tracked by DefiLlama. Currently not a meaningful competitor by volume.

Kyan Exchange: A new entrant building on Arbitrum with on-chain portfolio margin and multi-leg options support. In testing as of early 2026, not yet live at scale.

Hyperliquid: Not an options exchange perpetuals only. Included here because HYPE is the benchmark for what a decentralised derivatives exchange can become, generating $79.9M in fees over the past 30 days against Derive's $646K. Different product, same frame of reference.

GMX: Perpetuals DEX with $180M TVL and a different architecture. Does not compete directly on options but sits in the same category conversation.

Summary: Key Facts for DRV Tokenomics Research

Metric | Figure |

Max supply | 1,500,000,000 DRV |

Circulating supply (28 Jun 2026) | 737,520,000 DRV |

Market cap | $74.88M |

FDV | $152.3M |

Buyback allocation (current) | 35% of net protocol fees |

DRV repurchased (as of Mar 2026) | 21.3M+ (ongoing weekly) |

TVL (DefiLlama, Derive V2) | $109.3M |

Top 10 wallet concentration | 82.55% (Ethereum on-chain) |

Largest holder share | 53.65% |

Weekly trading rewards emission | ~50,000 DRV |

Max weekly staking emission (post-6 months) | 600,000 DRV |

Risks Worth Knowing

Supply overhang: 762M tokens remain to enter circulation from unlocks and emissions

Holder concentration: 82.55% of on-chain supply in 10 wallets introduces liquidity risk

Revenue dependency: Buybacks are not automatic. They require sustained trading volume

Governance control: Any parameter in this model including the 35% buyback allocation can be changed by a DAO vote

The supply cap was already raised once: In September 2025, co-founder Nick Forster proposed minting 500M additional DRV tokens, raising the supply cap from the original 1B to 1.5B, a 50% increase. Based on current CMC supply data showing the 1.5B ceiling, this proposal passed. The 1.5B cap is not the original hard cap; it is the result of a governance vote that expanded it. A future vote could expand it again

Market context: Coinbase acquired Deribit, the centralised options exchange that controls approximately 80% of global crypto options volume, for $2.9 billion in 2025, validating the market Derive is building in. This is the backdrop against which Derive's institutional growth narrative should be read

Data sourced from CoinMarketCap (28 June 2026), DefiLlama (Derive V2), Derive's published documentation at docs.derive.xyz and derive.xyz/drv, Derive's published buyback logs, and Derive's whitepaper (Kraken-hosted PDF). This article is for informational purposes only and does not constitute financial or investment advice.

Want a chart read on DRV? Coinjuice PRO covers technical setups across DeFi tokens using the QFL base structure method, the same framework used in the Coinjuice trading ebook. If you want to understand how to read accumulation and distribution zones before sizing a position, that is the place to start.

FAQ

What is Derive (DRV) and how does the platform work?

Derive is a decentralised derivatives exchange where users can trade options, perpetuals, and spot assets from self-custodied wallets. It runs as an optimistic rollup on the OP Stack settling to Ethereum, uses a Rust-powered off-chain orderbook with on-chain settlement capable of up to 20M TPS, and is designed for professional traders, institutions, and market makers.

How is the DRV token allocated and what is its maximum supply?

DRV is an ERC‑20 token on Ethereum with a maximum supply of 1.5 billion. At launch, 40% was allocated to community incentives, 25% to ecosystem development, 20% to a foundation reserve, and 15% to strategic partners and early investors. As of 28 June 2026, 737.52M DRV are circulating, with a market cap of $74.88M and an FDV of $152.3M.

How does the DRV buyback mechanism work and what changed in April 2026?

The DAO directs 35% of net protocol fees—earned from trading fees, liquidation fees, interest rate spreads, and Derive L2 rollup fees—to weekly DRV buybacks on decentralised exchanges. Over 21.3M DRV (about 2.9% of circulating supply) had been repurchased by March 2026. In April 2026, governance increased the buyback allocation from 25% to 35% of net fees and reduced weekly staking emissions from 250,000 to 100,000 DRV, directing more revenue to repurchases and slowing new supply from staking.

What are the main risks related to DRV tokenomics and holder distribution?

Key risks include a supply overhang of about 762M DRV still to enter circulation, high holder concentration with the top 10 Ethereum wallets holding 82.55% of on-chain supply and the largest wallet alone holding 53.65%, revenue dependency because buybacks require sustained trading volume, and governance control over parameters such as the 35% buyback allocation and even the total supply cap, which was already raised once from 1B to 1.5B DRV in 2025.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.