Quick summary

By 2026, Bitcoin functions primarily as a savings asset, while dollars continue to handle everyday transactions

This dual-money structure mirrors historical patterns, where reserve assets are hoarded faster than transactional currencies

Bitcoin shows its strongest adoption in remittances, internet-native activity, and regions with restricted banking access

The Lightning Network enables small, fast online payments, while structured savings strategies help manage Bitcoin’s price volatility

In 2026, living on Bitcoin is no longer theoretical but documented, region-specific, and increasingly organized around the Dual Money Era, where Bitcoin functions primarily as a savings technology while dollars continue to dominate everyday spending.

The dominant model is not a Bitcoin-only economy.

Instead, evidence points to a Dual Money reality, where Bitcoin functions primarily as a long-term store of value while the US dollar continues to dominate everyday transactions. This structure is the system working as designed.

Bitcoin as Savings, Dollars as Spending

River Financial’s Dual Money Era research outlines a historical pattern repeated across civilizations: the asset used to preserve wealth often differs from the currency used for daily exchange.

Gold and national currencies coexisted for centuries under similar dynamics.

Bitcoin is increasingly occupying the reserve asset role, while the dollar remains the unit of account and medium of exchange.

In practice, this means:

Bitcoin: Primarily used for long-term savings and balance sheet protection rather than day-to-day spending.

US Dollars: Remain the dominant unit for wages, rent, taxes, contracts, and price denomination.

Stablecoins: Commonly used as transactional bridges in regions with limited or unreliable access to dollar banking.

This structure reflects realism rather than compromise. Transactional currencies change slowly. Reserve assets can change within a generation.

People don’t need to replace how they spend money, in order to upgrade how they save it.

Everyday currencies, used for wages, rent, taxes, and pricing are deeply embedded in legal systems, contracts, and habits, so they change very slowly. Reserve assets, on the other hand, exist mainly to preserve value over time, and examples in history shows those can shift much faster when a better option appears.

Gold vs. National Currencies (Pre-1971)

For centuries, gold functioned as the primary reserve asset, while national currencies were used for everyday transactions.

Local Currencies: Used by households to earn income, price goods, pay wages, and conduct daily commerce.

Gold: Held by governments and institutions as the primary reserve asset for long-term savings and international settlement.

Velocity: Gold circulated infrequently compared to currency, reflecting its role in preservation rather than day-to-day exchange.

Throughout history, the asset most widely used for saving has differed from the currency used for transacting. Gold’s role as a reserve asset shifted much faster than the transactional currencies tied to it. Local money systems persisted even as the underlying savings asset changed.

The Bretton Woods Transition (1944–1971)

After World War II, the world moved from a gold-based reserve system to a dollar-backed reserve system, while everyday currency usage barely changed.

Everyday Currencies: Continued to be used locally for wages, pricing, taxes, and contracts with little disruption.

Reserve Layer: Shifted from gold to the US dollar as the primary asset held by governments and central banks.

Timeframe: The transition of the global reserve asset occurred within a single generation, while transactional habits remained intact.

People didn’t suddenly stop using francs, pounds, or yen in daily life. The reserve layer changed, not the spending layer.

Argentina (Ongoing, Multi-Decade Example)

Argentina’s peso remained the transactional currency despite repeated inflation crises, while savings behavior shifted away from pesos.

Argentinians know better than to save their wealth in pesos. Despite all this, the Argentine peso remains the primary way to earn wages, transact, and denominate wealth. Savings moved into dollars, real estate, stocks, and hard assets.

Wages, pricing, taxes, and contracts remained anchored to the existing currency and grew gradually over time. This illustrates how saving behavior can shift to a new reserve asset without requiring a parallel replacement of the transactional currency, mirroring the current Bitcoin dollar dynamic.

What History Shows About Bitcoin

History shows that societies upgrade how they store value long before they replace how they transact. Reserve assets change when they fail to preserve purchasing power, while transactional currencies persist due to legal, social, and network effects.

Bitcoin fits this reserve-asset role, allowing savings behavior to increase without disrupting daily economic life, making gradual adoption a strength rather than a weakness.

Where Bitcoin Fits Into Daily Life in 2026

Bitcoin’s strongest traction as a medium of exchange appears in specific contexts, not across entire economies.

River’s research highlights several areas where Bitcoin has already reached practical product–market fit:

Cross-Border Payments: Used where transfer speed and cost efficiency are needed, especially for remittances.

Internet-Native Activity: Adopted for gaming, tipping, streaming, and other digital-first transactions.

Restricted Dollar Access: Utilized in regions facing capital controls, sanctions, or limited banking access.

In El Salvador, Bitcoin’s legal tender experiment has largely shifted into a voluntary, state-supported framework, with the government holding appriximately seven thousand BTC in reserve while everyday use remains limited. Most Salvadorans continue to conduct daily transactions in dollars, and Bitcoin’s role in remittances and local payments has remained modest.

As of recent reporting, adoption primarily exists in specific communities like El Zonte (“Bitcoin Beach”) and among crypto-engaged individuals rather than widespread retail usage

In countries such as Nigeria, Bitcoin usage concentrates on income preservation and remittances, rather than in-person retail payments.

Peer-to-peer activity thrives where banking access is constrained, while local currencies remain dominant for everyday spending. In Kenya, specifically the slum area of Kibera, here it illustrates how Bitcoin adoption emerges not from speculation, but from necessity and prior experimentation.

In Nairobi’s Kibera, particularly the Soweto West neighborhood, Bitcoin is being used by a small but growing group of residents for everyday transactions such as buying vegetables, paying informal workers, and receiving remittances.

This shift has been supported by local fintech initiatives like AfriBit Africa and builds on earlier community finance systems such as Sarafu-Credit, which familiarized residents with mobile, trust-based value exchange long before Bitcoin arrived.

In an environment marked by limited bank access, security risks associated with cash, and high remittance costs, Bitcoin functions as a practical complement to tools like M-Pesa rather than a replacement, offering greater autonomy, reduced reliance on physical cash, and an alternative savings mechanism where traditional financial systems fall short.

In higher-income economies, Bitcoin often appears as financial optionality, held as savings, integrated into payroll services, or accessed through investment platforms while daily life continues to run on fiat rails.

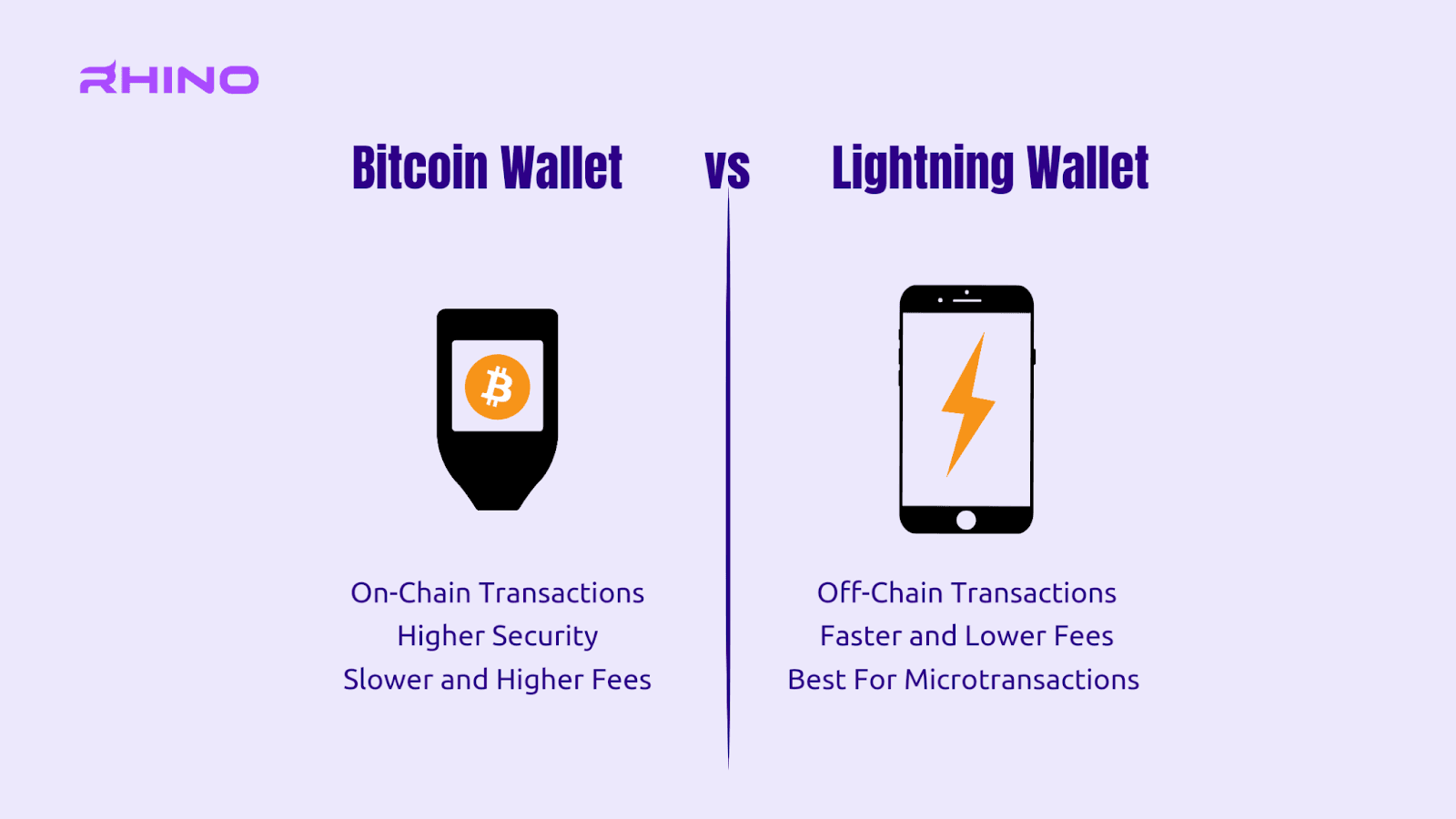

The Role of the Lightning Network

Lightning has not emerged as a universal replacement for existing payment systems and that was never the real test. Its traction shows up elsewhere: in fast, low-value, high-frequency transactions, especially online.

What stands out in practice:

Transaction Size: A large share of Lightning activity consists of very small, high-frequency payments.

Use Cases: Adoption clusters around remittances, digital services, and internet-native activity.

System Fit: Lightning operates alongside dollar-based payment systems rather than attempting to replace them.

This reinforces the broader pattern already visible across Bitcoin usage: new financial capability is added without forcing abrupt change. Expansion happens at the edges first, where speed, cost, and permissionless access matter most.

Volatility and the Long View

Bitcoin volatility remains part of the picture. That reality has not disappeared in 2026, but it has become better understood and more deliberately managed.

Savings Separation: Long-term Bitcoin holdings are kept distinct from funds intended for daily spending.

Conversion Discipline: Bitcoin is converted based on practical needs rather than short-term price movements.

Functional Mindset: Bitcoin is approached as financial infrastructure, not a vehicle for speculation or entertainment.

This behavior is not new. It mirrors how individuals and institutions historically interacted with gold, foreign currencies, and inflation hedges assets held for durability, not daily usage.

Sustaining the Dual-Money Structure

Bitcoin continues to gain relevance where existing financial systems fall short:

Inflation protection: Preserving purchasing power in environments of sustained currency debasement.

Cross-border mobility: Moving value across borders quickly and efficiently.

Financial access: Operating independently of fragile, restrictive, or exclusionary banking systems.

Adoption advances where problems are real and solutions are practical. Bitcoin does not need to replace the dollar to justify its role as a store of value. Bitcoin needs to succeed precisely where the dollar struggles.

Conclusion

In 2026, living on Bitcoin is no longer framed by theory or ideology, but by structure and use. The evidence points to a clear pattern: people adopt Bitcoin where it improves outcomes, while established currencies continue to handle everyday economic activity. This balance allows savings behavior to grow without forcing disruption to wages, pricing, or contracts.

History shows that monetary systems rarely change all at once. Reserve assets shift first, transactional currencies later, if at all. Bitcoin’s role follows this pattern closely, functioning as a long-term store of value alongside existing payment systems rather than attempting to replace them outright.

As this structure becomes better understood, attention naturally turns to execution: managing volatility, earning income, and moving between systems efficiently. Those questions build on a foundation that is already visible today.

The future of Bitcoin usage is shaped less by maximalism and more by intent, structure, and patience.

FAQ

What does the Dual Money reality look like in 2026?

Bitcoin is used primarily as a long-term savings and balance sheet protection asset, while the US dollar remains dominant for wages, rent, taxes, contracts, and price denomination. Stablecoins are commonly used as transactional bridges where access to dollar banking is limited. This reflects a structure where reserve assets can change within a generation, while transactional currencies change slowly.

How do historical examples like gold, Bretton Woods, and Argentina relate to Bitcoin’s role today?

Historically, the asset used for saving has often differed from the currency used for daily transactions. Gold served as the main reserve asset while local currencies handled everyday commerce, and after World War II the reserve layer shifted from gold to the US dollar without changing local currency use. In Argentina, the peso remains the transactional currency while savings move into dollars and hard assets. These patterns mirror Bitcoin’s emergence as a reserve-style savings asset alongside existing currencies.

Where has Bitcoin reached practical product–market fit as a medium of exchange by 2026?

Bitcoin sees its strongest traction in cross-border payments (especially remittances), internet-native activity such as gaming, tipping, and streaming, and in regions with capital controls, sanctions, or limited banking access. For example, it accounts for roughly 1% of remittance volume into El Salvador while most prices remain in dollars, and in countries like Nigeria it is used mainly for income preservation and remittances while local currencies dominate in-person retail payments.

What is the role of the Lightning Network and how is Bitcoin’s volatility managed in daily life?

The Lightning Network is used for fast, low-value, high-frequency Bitcoin transactions, especially online, clustering around remittances, digital services, and internet-native activity. It operates alongside dollar-based payment systems rather than replacing them. Bitcoin’s volatility is managed by keeping long-term holdings separate from daily spending funds, converting based on practical needs instead of short-term price moves, and treating Bitcoin as financial infrastructure rather than a speculative tool.

Disclaimer

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Written by

Andrew Kamsky

Andrew Kamsky is a Bitcoin analyst. He spent a decade in traditional finance across a Big Four firm and a listed fintech bank before going deep on Bitcoin full-time.